Although the coronavirus pandemic delivered a staggering blow to the global economy, the central issue now is whether the market rallies got ahead of themselves.

Although the coronavirus pandemic delivered a staggering blow to the global economy, equity and credit markets rallied dramatically in the second quarter through mid‑June. The central issue now is whether those rallies have gotten ahead of themselves, Sharps says.

“Anytime you’re in an economic downturn, there comes a point where markets begin to anticipate improvement,” Sharps notes. “Given that the spread of the virus appears to have slowed and many businesses are reopening, I’m not too surprised that markets are off their lows.”

Recent signs that U.S. employment is bouncing back more rapidly than expected as the economy gradually recovers are a significant “green shoot” that has pushed yields on 10‑ and 30‑year Treasury bonds modestly higher, Vaselkiv notes.

That said, the near‑term earnings outlook remains grim. While consensus forecasts at the start of the year anticipated global economic growth of around 3%, current estimates see a 3% decline for the year, Thomson says. Taking operating leverage into account, that could produce a 50% to 60% aggregate decline in corporate profits.

“We’re still very early in the recovery,” Sharps warns, “but I do think the second quarter will prove to have been the most challenging for economic activity and earnings.”

The key question, Sharps says, is how long it will take for companies to regain enough earnings power to justify current valuation levels while compensating investors for the risk that an economic recovery might not progress as rapidly or evenly as expected.

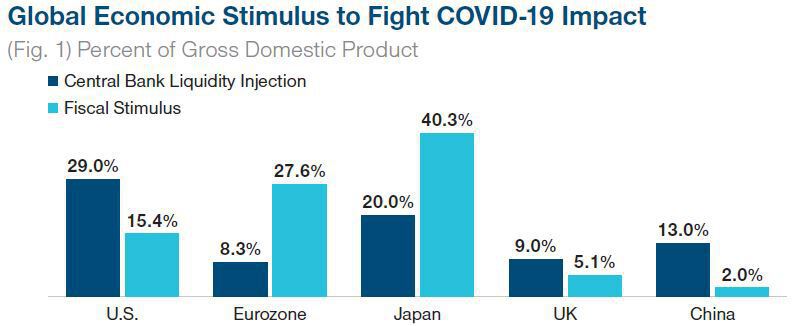

To a large extent, the rally in risk assets has been driven by massive doses of fiscal and monetary stimulus, which have been even larger than during the 2008–2009 global financial crisis. This, Thomson says, has set the stage for a tug of war between ample liquidity and the collapse in earnings. Further market volatility could result, he cautions. While fiscal and monetary stimulus have bolstered global markets, there are limits to what governments can do to sustain the recovery:

January 31 through May 31, 2020 Sources: Cornerstone Macro, used with permission. Additional T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

With much of the anticipated benefits of stimulus already priced into risk assets, economic fundamentals will have to take over for broad markets to move higher, Sharps says. “I think the going will be tougher from here.”