The economic and social consequences of the pandemic appear to have accelerated the rise of dominant technology platforms.

The economic and social consequences of the pandemic appear to have accelerated the rise of dominant technology platforms in retail, social media, streaming content, and remote conferencing. This trend is likely to widen the divide between industries and companies benefiting from disruption and those challenged by it.

T. Rowe Price analysts are carefully assessing companies to identify the ones they believe have the balance‑sheet strength to get to the other side of the pandemic and how that could impact recoveries in equity and credit markets.

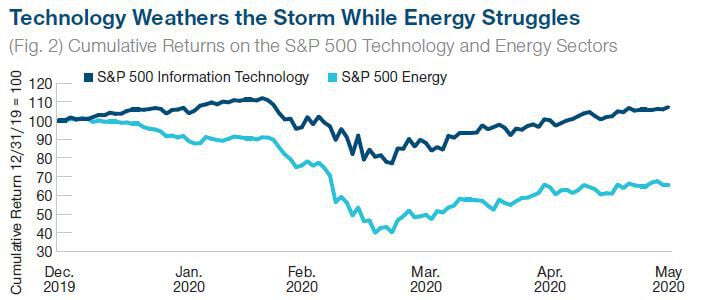

“The changes over the past few months in the ways we work, socialize, and entertain ourselves have advanced the fundamentals of the big tech platform companies by several years,” Sharps says. Through the first five months of 2020, Sharp notes, technology was the strongest performing sector in the S&P 500 Index while energy—hurt by collapsing demand and a price war between Russia and Saudi Arabia—was the worst performing.

The largest of the mega‑cap technology giants appear well‑positioned to benefit from accelerating disruption, according to Sharps.

Going forward, Sharps suggests, disruption and the pandemic both should continue to favor the top five U.S. technology platforms, which, as of early June, already accounted for more than 20% of market capitalization in the S&P 500 Index—greater than the bottom 340 index constituents combined.

Past performance is not a reliable indicator of future performance.

December 31, 2019, through May 31, 2020. Sources: T. Rowe Price calculations using data from FactSet Research Systems Inc. All rights reserved. J.P. Morgan Chase & Co., Bloomberg Finance L.P., and Standard & Poor’s (see Additional Disclosures).

Meanwhile, a number of sectors with heavy weights in the value universe—such as energy, transportation, and financials—have been deeply damaged by the crisis. “Large parts of the market still haven’t recovered yet,” Thomson says.

While better‑than‑expected economic news prompted a shift back toward some challenged sectors—growth to value, large‑cap to small‑cap, and U.S. to non‑U.S. equities—in early June, a more sustained reversion trade will require an uptick in inflation and a weaker U.S. dollar, Thomson argues.