The economic damage wrought by the coronavirus pushed credit quality into the spotlight in the first half of 2020.

The economic damage wrought by the coronavirus pushed credit quality into the spotlight in the first half of 2020, as fixed income investors sought shelter in sovereign debt and other top investment‑grade (IG) assets.

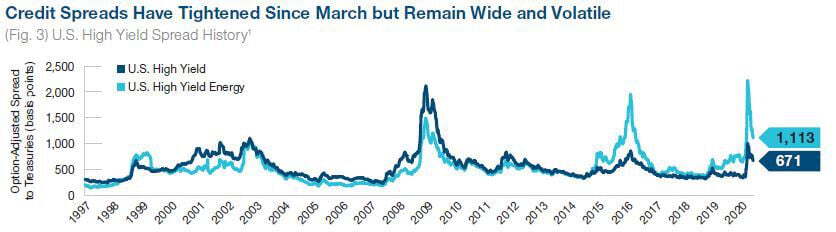

While credit spreads have narrowed from the worst of the market sell‑off in March, they remain wide and volatile, Vaselkiv notes. However, as in global equity markets, performance has been highly uneven.

In the high yield market, yield spreads for BB rated bonds perceived as defensive have tightened to pre‑crisis levels. Yet, some “fallen angels”—companies that have recently lost their IG ratings—have been forced to sell bonds with yields as high as 9% to shore up their balance sheets. In this environment, investors need to carefully analyze relative value on a case‑by‑case basis, Vaselkiv says. In forecasting potential default rates, T. Rowe Price analysts have divided the high yield universe into three broad groups, Vaselkiv says:

Many fixed income managers already have rotated into well‑positioned sectors and now are cautiously expanding their cyclical exposures, Vaselkiv says. How that latter category fares in the recovery will determine the peak default rate for the high yield universe as a whole. An aggregate rate close to 10% appears warranted, he adds.

Past performance is not a reliable indicator of future performance.

January 1, 1997, through May 31, 2020. Sources: Bloomberg Index Services Limited, and ICE BofAML (see Additional Disclosures). T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved. 1 U.S. High Yield = ICE BofA US High Yield Index. U.S. High Yield Energy = ICE BofA US High Yield Energy Index.

Attractive fixed income opportunities in the second half appear relatively limited, in Vaselkiv’s view. Defensive assets, such as U.S. Treasuries and other developed sovereigns, AAA rated munis, and even some high‑quality securitized sectors, are expensive and vulnerable to a further backup in interest rates if the recovery proves faster than expected and/or a vaccine becomes widely available. In emerging fixed income markets, some specific opportunities appear attractive, but the sector as a whole remains under severe pressure from the pandemic and, in some countries, such as Brazil, from poor political leadership, Vaselkiv says. Sovereign default rates have risen.