While the coronavirus crisis dominated the policy agenda in early 2020, investors will need to monitor a host of other risks including social unrest, opposition to economic globalisation, and US elections scheduled in November.

While the coronavirus crisis dominated the policy agenda in early 2020, investors will need to monitor a host of other risks—some potentially worsened by the pandemic—in the second half. These include rising tensions between the U.S. and China, social unrest, opposition to economic globalization, and U.S. elections scheduled in November.

Even before the coronavirus disrupted their operations, the ability of multinational firms to exploit global economies of scale was being challenged by protectionist pressure, Sharps notes. Now, after seeing the pandemic play havoc with supply chains, corporate managers themselves are likely to emphasize resilience over efficiency, even if it lowers profit margins.

The economic benefits are too compelling for globalization to go into reverse, Sharps contends. “But if you add in the ongoing trade tensions between the U.S. and China, a trend toward reevaluating global supply chains seems inevitable.”

Thomson says he is optimistic that the U.S. and China will step back from an escalation in their trade war, easing one potential threat to the global economic recovery. However, he predicts a longer‑term competition for dominance in key technology sectors is likely to produce continued friction between the two economic giants.

Hong Kong, China’s special administrative region, is caught in the middle of these tensions, Thomson says. However, while western critics decry Beijing’s efforts to push through a new security law for the city, Thomson predicts that China will not impose its legal framework directly on Hong Kong as that would threaten the city’s viability as a financial center.

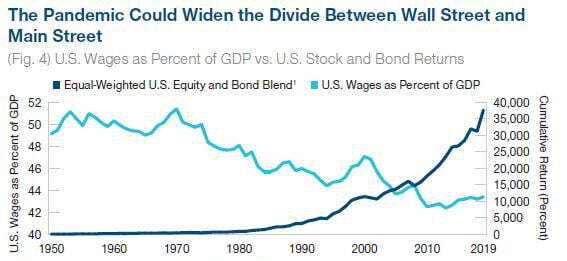

High unemployment, social distancing, and the digital divide between those able to work from home and those who’ve seen their incomes destroyed by the coronavirus all could worsen a long‑running shift toward income inequality in the U.S. and other developed countries.

Vaselkiv notes that the pandemic has been especially damaging for lower‑income workers in the service sector, many of them women and/or people of color. This has added to anger over racial injustice and claims of widespread police brutality that have prompted mass protests in many U.S. cities.

Past performance is not a reliable indicator of future performance.

January 1, 1950, through December 31, 2019. Sources: FactSet, Standard & Poor’s, Bureau of Economic Analysis, Federal Reserve Board, Tax Policy Center, and Citizens for Tax Justice/Haver Analytics (see Additional Disclosures). 1 Equal‑weighted total return of U.S. equities (S&P 500 Index) and U.S.10‑year government bonds.

The upcoming U.S. election also poses risks for markets, Sharps warns. A victory by Democrat Joe Biden, he says, could lead to increases in both corporate and individual taxes, especially if the Democrats also take control of the Senate. Tighter regulation under a Biden administration could impose heavy compliance costs on energy, financials, and some manufacturing industries, Sharps adds.

Looking ahead to the second half of 2020, investors should expect more gradual recoveries in risk assets—not a continuation of the powerful rallies that lifted markets off their March lows, the three T. Rowe Price leaders say.

“There are still potential opportunities, but they’re clearly less compelling than they were in April,” Sharps says.

Thomson says he is relatively optimistic about the second half outlook, although markets could be “choppy” at times. “I think reopening economies, plus the scale of the stimulus and the potential for medical breakthroughs, create the potential for stocks to move higher between now and the end of the year,” he predicts.

But in a fast‑changing environment, investors will need to be able to generate fundamental insights, look at the full opportunity set within sectors and industries, and prioritize the most attractive opportunities in order to be successful, Sharps observes.

A long‑term investment perspective and close attention to potential risks also could be critical. “It took over a decade for economies to recover fully from the global financial crisis,” Vaselkiv notes, “and we’re facing even bigger challenges today. So I would encourage investors to carefully monitor the risk exposures in their portfolios.”