Equity markets to broaden

further

Equity Outlook

Head of Global Equity

Portfolio Manager, Global Equity

An expanding opportunity set in stock markets was on its way before Donald Trump was elected US president; the trade policies he has implemented since taking up office have merely sped up the process. This expansion of investable stocks will take place both within the US market and abroad. We are returning to an environment in which more sectors and regions can work—one demanding diversification and favouring active management.

Broadening market leadership has already begun to occur: Many overseas stock markets have outperformed their US counterparts this year. This expansion of leadership should continue in the second half of the year. Although the Trump administration’s tax cut and deregulation agenda will deliver a boost to the US economy, this will likely be balanced out in the near term by ongoing uncertainty over tariffs and their impact on US consumers and businesses.

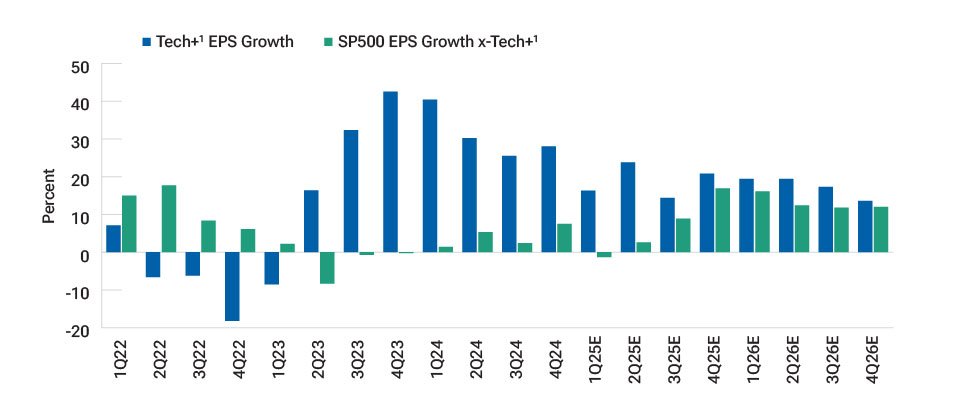

At the same time, the era in which the “Magnificent Seven” group of mega‑cap tech stocks dominated the S&P 500, and by extension helped US stocks to dominate the world, could be transitioning to a new phase where a broader cross‑section of stocks outperform. The spread of earnings growth between technology stocks and the rest of the S&P 500 has been narrowing, and we expect this to continue (Figure 2). The emergence of start‑ups such as China’s DeepSeek are showing that AI innovation is no longer concentrated in a handful of trillion‑dollar companies.

As US inflation remains higher for longer, value stocks—which historically have outperformed growth stocks in inflationary environments—are expected to become more competitive again. Value sectors such as energy, materials, and industrials historically have performed well during inflationary periods.

Opportunities for regional diversification are likely to come mainly in EM countries. Of these, India looks well positioned after two terms under Prime Minister Narendra Modi have delivered solid economic growth, reforms, and investment. With its large, domestically driven economy, India is more insulated from tariff‑related volatility than many of its rivals and has sufficient critical mass—measured in economic scale, infrastructure, digital adoption, and the expansion of the middle class—to continue its growth path. While Indian stock valuations remain elevated, the market’s resilience and strong economic fundamentals should not be underestimated if buying opportunities occur.

Germany’s decision to end its longstanding debt brake will enable increased investment.…

Argentina continues to catch the eye amid ongoing reforms under President Javier Milei. His administration’s efforts to balance the budget and control inflation have helped to transform Argentina’s economic prospects, which have been further boosted by a USD 20 billion loan from the International Monetary Fund. The risk premium associated with Argentine stocks means they remain attractively valued, offering discounts compared with some of their regional peers.

Indonesian and Saudi Arabian stocks are also expected to perform well as part of a broader tilt toward international equities. However, some other countries, notably Vietnam, face a somewhat more challenging period ahead as they navigate US‑China tensions.

Outside of emerging markets, European stocks have outperformed US stocks this year and appear well placed to continue doing so. European equities are trading at lower price‑to‑earnings ratios than their US counterparts and are more likely to benefit from a central bank rate cut. Germany’s decision to end its longstanding debt brake will enable increased investment and defence spending, while the prospect of reduced trade with the US might persuade the European Union to introduce much‑needed reforms.

One area to monitor is the fluid situation with tariffs, as shown in the US’s decision on May 23 to impose a 50% rate on European Union goods only to postpone it a few days later. The size, scope, and speed of tariff implementation could bring further volatility for both US and European stocks.

Finally, while Japan has been hit harder than Europe by Trump’s tariffs given its greater dependence on exports to the US, Japanese stocks appear undervalued compared with historical norms and global peers. Japan’s strong underlying fundamentals—including a robust corporate sector, high savings rates, ongoing corporate governance reforms, and the return of positive inflation—remain in place and will be supportive, particularly if it strikes a favourable trade deal with the US

As equity market leadership becomes less concentrated, the mix of opportunities will likely broaden across sectors and countries. Successfully navigating this environment will require diversification1 and a renewed focus on identifying high‑quality companies. A broader market provides more opportunities, but it also brings additional risk.

1 Diversification cannot assure a profit or protect against loss in a declining market.

(Fig. 2) The spread of earnings growth between tech and other sectors is narrowing

The broadening of equity market leadership should favour value stocks and select emerging markets such as India and Argentina.

In this video, Jennifer O'Hara Martin, Portfolio Specialist in Global Equity, explains how the expansion of equity markets, driven by the new administration’s trade and national security policies, is significantly impacting capital flows.