Inflation protection and equity diversification to drive asset allocation

Asset Allocation

Capital Markets Strategist

While we anticipated a deglobalisation process following the pandemic‑induced supply chain snarls in 2020, the threat of tariffs has brought globalisation under attack. Countries and companies are scrambling to reduce their exposure to tariffs, greatly accelerating the deglobalisation trend. This process will have significant implications for asset allocation as some previously favoured assets become less attractive and others show more potential.

One thing is clear—the Federal Reserve will stick to its data‑dependent approach, avoiding forward guidance, and continue to assiduously avoid any messaging that could be interpreted as political. Fed policymakers know that lower rates are not a cure for uncertainty, so we do not expect a “Fed put” in the form of an interest rate cut over the near term. We see little chance that the central bank will lower rates until a major increase in the unemployment rate shows that a recession is obviously imminent.

The Fed is also reluctant to cut rates because of the risk that tariffs will pressure inflation higher. We are mindful of this possibility and favour exposure to inflation protected bonds and real assets like real estate and commodities as tools to help offset inflation risk. Our Asset Allocation Committee (AAC) holds an underweight position in longer‑term US Treasuries as they could underperform amid resurgent inflation. Additionally, Treasuries face growing scrutiny from foreign investors due to concerns about fiscal sustainability and economic policy uncertainty.

In times of rapid geopolitical change, we tend to lean more heavily than usual on asset class valuations. Even after the concentrated selling pressure on growth stocks and value’s relative outperformance in early 2025, value equities appear to provide more valuation support than growth.

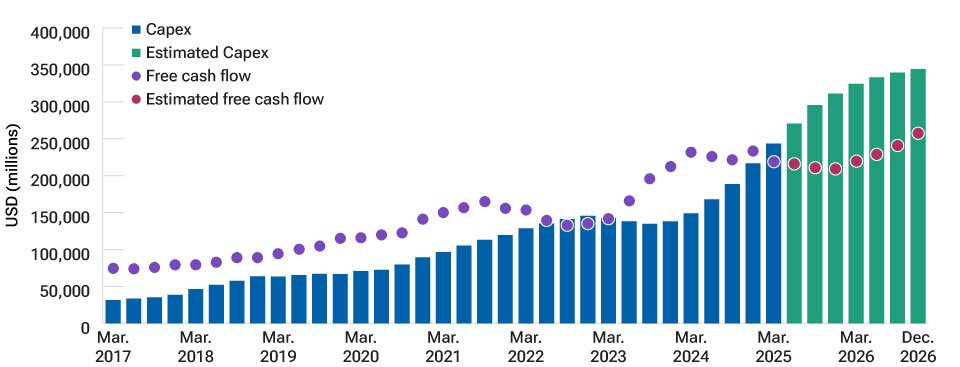

In artificial intelligence, the tremendous advantages of being on the right side of change, as illustrated during the shifts toward digital media, online retail, and cloud computing, appear to have flattened out. As a result, the tech giants are spending heavily on AI to try to ensure they maintain their positions on the leading edge of technology. We believe this spending will profitable over the longer term, but time horizon is important. These innovative firms could see their valuations challenged over the near term by flattening returns on equity while their capital expenditures are elevated (Figure 4).

In a typical economic growth downturn or recession, we would expect US equities to hold up better than international stocks. But we believe the underlying dynamics of this year’s slump may be different, leading us to modestly favour non‑US shares.

One factor working against US equities is the inflationary pressure from tariffs that will keep the Fed on hold unless a recession is inevitable. Outside the US (and Japan, where the Bank of Japan has been gradually raising rates), central banks have more leeway to lower rates—and mortgage rates are more responsive to cuts, so the benefits flow through the economy faster.

Finally, the recent landmark decision by Germany to loosen its debt brake on defence spending and create a EUR 500 billion infrastructure fund is a dramatic change after more than a decade of austerity measures. This pivot could eventually provide a much‑needed fiscal boost to the European economy, which has been operating below capacity for most of the past 15 years, supporting the Continent’s equity markets.

All of these factors, combined with the sizable weighting of the mega‑cap tech firms in growth stock indexes, led the AAC to a relative underweight to US growth equities.

Japan still stands out among international equity markets because of its positive momentum toward stronger corporate governance. The country’s steady progress toward a healthy level of inflation and domestic consumption should also support its stock market. While exports are a major driver of Japan’s economy, making it particularly sensitive to US tariffs, Japan appears motivated to negotiate with the Trump administration to lower tariffs.

(Fig. 4) Capex vs. free cash flow for Microsoft, Alphabet, Amazon, and Meta, collectively

Our Asset Allocation Committee holds underweight positions in both long-term US Treasuries and US stocks.

Sébastien Page CFA®, Head of Global Multi-Asset and Chief Investment Officer, discusses the risk of surprises on inflation and how attractive valuations may lead us to favour international and value equities when determining portfolio allocations.