Bond investors may want to consider raising exposure to sectors, such as EM debt or U.S. government debt, that historically have done well late in the late-cycle.

Bond investors may want to consider raising exposure to sectors, such as EM debt or U.S. government debt, that historically have done well late in the cycle.

Longer-duration U.S. Treasuries have reached relatively attractive yield levels, so it may be a smart defensive posture in 2019.

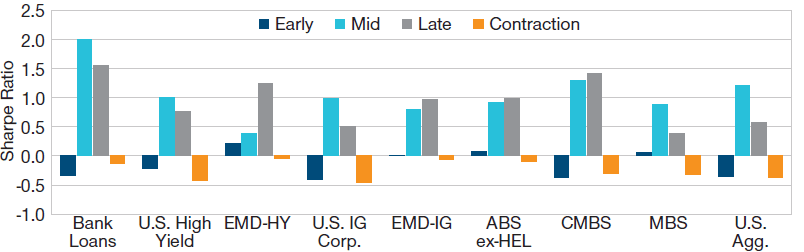

Historically, bond market sectors have shown varying return patterns over the economic cycle. As the U.S. economy moves into the later stages of that cycle in 2019, McCormick says, some sectors may offer attractive relative value opportunities. “In the middle of the cycle, the aggregate bond indexes typically have had very positive risk‑adjusted returns,” McCormick notes. “Bond returns tend to decrease in the late cycle. They’re not necessarily negative, but you don’t get paid as much for taking risk.” McCormick points to several sectors that historically have featured relatively strong late‑cycle performance. These include: Floating-Rate Bank Loans, Collateralized Loan Obligations, Emerging Markets Debt, Short-Duration Treasuries and Investment-Grade Corporates.

Floating-Rate Bank Loans: In 2018, strong U.S. growth supported credit fundamentals, while U.S. floating rates, as measured by London Interbank Offered Rates (LIBOR), rose in line with Fed rate hikes. As long as credit conditions remain favorable, bank loans should continue to perform relatively well, even if the Fed pauses raising rates. However, the sector’s bull run has stretched valuations and raised concerns about underwriting standards, requiring careful credit analysis by investors.

Collateralized Loan Obligations (CLOs): These floating rate instruments typically carry AAA ratings from the major credit agencies and historically have traded at yield spreads over LIBOR comparable to lower‑quality investment‑grade (IG) corporate bonds. Their short-duration profile and structural credit enhancements make CLOs attractive, especially as the end of the credit cycle approaches, McCormick says.

EM Debt: Historically, corporate and sovereign EM bonds both have outperformed late in the U.S. credit cycle, typically because the U.S. dollar has started to depreciate, boosting commodity prices and easing financial conditions in EM economies.

Short-Duration Treasuries and IG Corporates: Investors who did well with riskier assets in 2018 now have an opportunity to earn relatively attractive yields at the less volatile short end of the U.S. yield curve, McCormick says.

Giroux recommends that investors also consider another, relatively battered, fixed income sector: U.S. Treasuries. Although they performed poorly in the strong growth/rising rate environment of 2017 and 2018, longer‑duration Treasuries have reached relatively attractive yield levels, Giroux says, especially compared with comparable sovereign assets, such as German bunds and Japanese government bonds.

BONDS ARE MOVING FROM MID- TO LATE CYCLE Sharpe Ratio of Excess Returns As of October 31, 2018*

Sources: Federal Reserve, Goldman Sachs, and Bloomberg Finance LP; all data analysis by T. Rowe Price. *Based on excess returns versus similar‑duration Treasuries. Sector returns since January 1994, except for CMBS, which begins January 2000, and EMD-IG, which begins January 1998. Late cycle = market environment where either: economic growth is accelerating and Fed policy is tight, with tight policy defined as a real federal funds rate above both the Williams‑Laubach neutral rate and its own 12‑month moving average; or economic growth is falling and the Fed is tightening policy, with tightening policy defined as a real federal funds rate below the Williams‑Laubach neutral rate but above its own 12‑month moving average.