Widespread weakness in economic data confirms that global growth is moderating. As the tailwind from fiscal stimulus fades in the U.S., elevated uncertainty has discouraged spending and the anticipated boost to long-term growth through capital expenditure has failed to materialize. The Federal Reserve has paused additional interest rate hikes for now, with policymakers stressing that they will consider inflation and growth data to ascertain the need for any future rate changes. Growth in Europe has weakened, as the region’s vulnerability to trade risks and China’s slowing economy becomes apparent. Unresolved Brexit negotiations, the outcome of the recent European parliamentary elections—which reaffirmed the polarized and fragmented political environment—and the upcoming leadership transition at the European Central Bank also pose potential headwinds. China’s economic outlook remains a concern, as trade tensions with the U.S. linger and stimulus efforts have not yet stabilized growth. A full recession still appears unlikely, and selective opportunities remain, especially for active managers. While volatility has returned to markets amid concerns about trade wars and the global

Global Asset Allocation Views

• We have scaled back our exposure to global equities given economic weakness, the shaky global growth outlook, and elevated political and trade uncertainty. Fixed income yields are attractive amid moderating growth, are supported by favorable credit fundamentals, and may provide a buffer against equity market volatility.

• We have tapered our overweight allocation to international equities given rising risks from trade tensions and their exposure

to slowing global manufacturing.

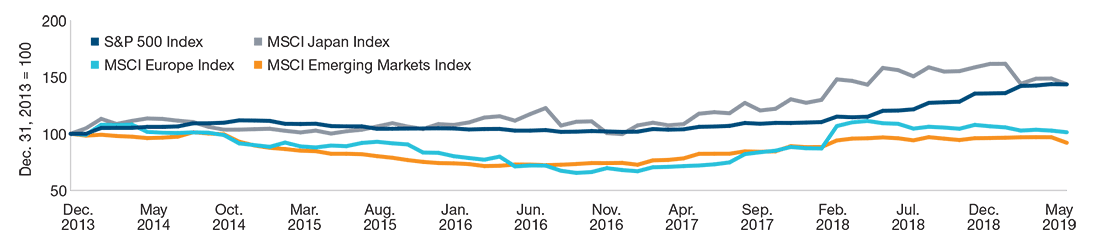

Sources: Standard & Poor’s (see Additional Disclosures) and MSCI (see Additional Disclosures). T. Rowe Price calculations using data from FactSet Research Systems Inc. All rights reserved.