We define secular disruption as the emergence of a new competitive force, technological advance, change in customer habit, or regulatory change that can substantially undermine a company’s long‑term growth potential. The effects of secular disruption are being felt in several sectors and industries, including autos, cable, gaming, publishing, mining, broadcasting, and retailing, to name a few. Our equity analysts estimate that about 31% of the U.S. stock market is affected by secular risk, compared with about 20% just two years ago. This is creating disparity among winners on the right side of change and losers that face slower topline growth rates, margin depression, and/or compressed multiples. While observers typically associate disruption with equity investing, meaningful change also exists in the credit markets where investors have more flexibility to invest in companies that may ultimately face disruptive challenges. At the same time,

Russell (see Additional Disclosures). T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

Global Asset Allocation Views

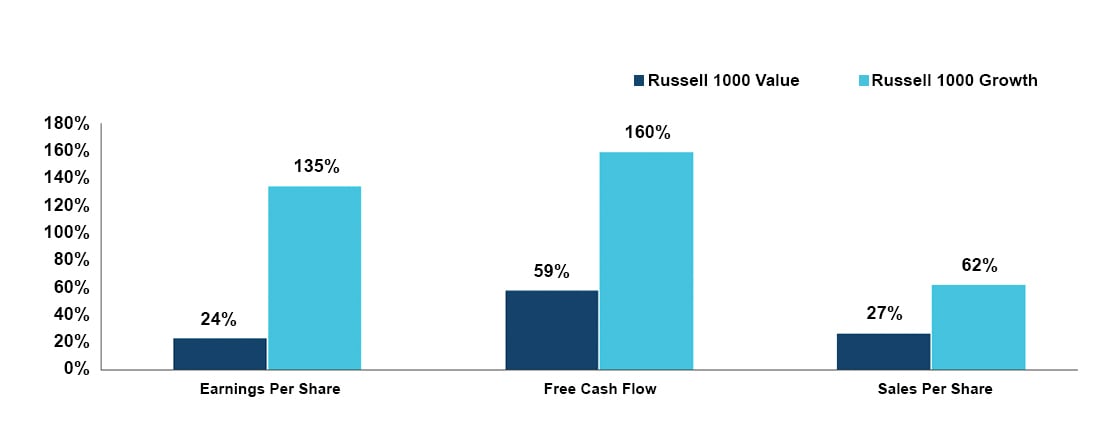

• We are overweight U.S. growth stocks. Secular growth companies—which are primarily concentrated in the U.S. and emerging Asia—may benefit even in a slowing economic environment. Despite fair valuations, many value sectors lack a catalyst to advance and are highly sensitive to economic downturns, while others face challenges from the emergence of new disruptive forces.

• We are underweight international value stocks as broad economic weakness poses a near-term challenge, particularly within cyclical sectors. Persistent low interest rates and fundamental weakness among European financials—a key barometer of the value sector—also pose headwinds.