Monetary expectations have shifted dramatically since the beginning of the year, with several central banks across the globe now expected to cut rates.

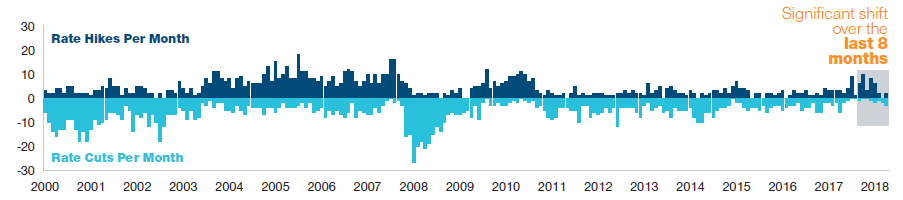

After a long period of unwinding, 2019 has seen a number of central banks, including the Federal Reserve, hit the pause button on interest rate hikes. A major reason for late 2018 sell‑off was concern over excessive monetary tightening. The pause was welcome news to global markets, and there are increasing expectations the Fed will further pivot to stimulus. However, policymakers need to walk a fine line to avoid a monetary policy misstep that would result in unintended turmoil. Elsewhere, China is implementing stimulus measures to help combat the economic impact of the trade conflict and fading growth. The European Central Bank, following a series of weak economic data, signaled that rates would remain at current levels at least until the end of 2019 and a readiness to take further action if needed. The Bank of Japan would also like to be more accommodative to support its lagging economy. The combined stimulus efforts from the U.S., China, and the eurozone could extend the long-running risk rally. However, current tariff tensions reinforce the view that central banks of developed market countries may have to become more accommodative.

Central Banks No Longer in Tightening Mode, As of May 14, 2019

Source: BIS Central Bank Policy Rates. Analysis by T. Rowe Price.

• Within our fixed income allocation, we are overweight to emerging markets debt, which broadly offer attractive yields and typically benefit from a dovish central bank environment. However, country-specific risks are on the rise with heightened political uncertainty in several key markets. • We have increased our allocation to high yield bonds, which offer a yield advantage supported by healthy corporate fundamentals with low default expectations. Relative to equities, high yield bonds currently offer similar return expectations with a lower volatility profile.