Over the past three years, 59% of plans note they have had no change to their overall foreign fixed income allocation, whereas 28% have increased their overall allocation to foreign fixed income. This movement to global fixed income is an appropriate and prudent re-allocation and consistent with what we think will take place in the coming years. When asked what drives changes to foreign fixed income allocations, most respondents cited seeking higher returns as the top choice (34%), followed by de-risking (16%) and increasing diversification (13%) (See Figure 3 below)

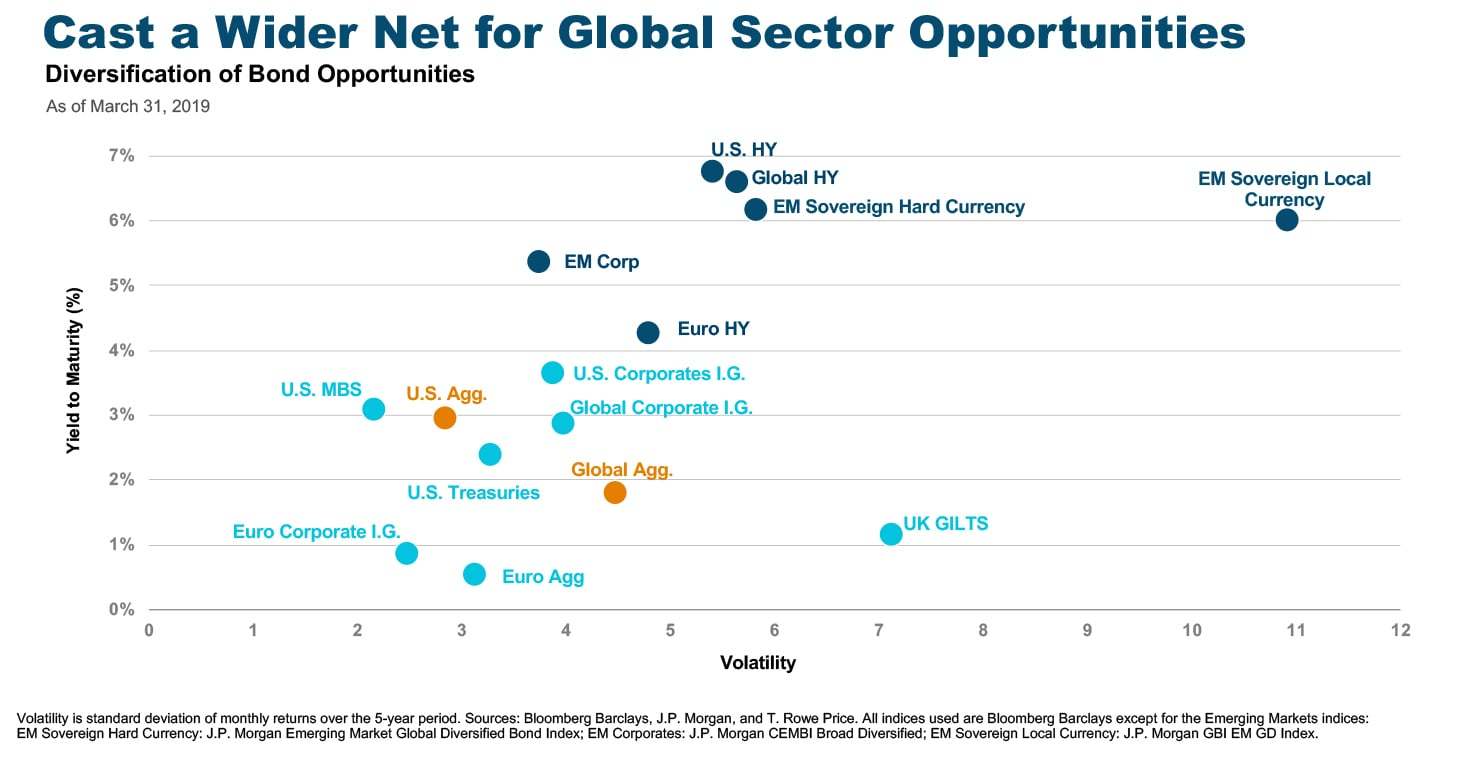

A Closer Look at Emerging Markets Depending on the strategy, emerging markets can offer plan sponsors a way to meet assumptions with a minimal to moderate increase in risk. Evidence of the potential benefits of emerging markets can be seen in the ‘Cast a wider net’ chart, where over the past 5 years (as of 29 March 2019), emerging market fixed income investments have provided a much higher yield than more traditional strategies while also carrying an overall investment grade rating. For example, the 2.6% yield of the Canadian Aggregate pales in comparison to the 4.5-6% yields from emerging market opportunities.

Survey results suggest that plan sponsors do recognize the potential for emerging markets, as 28% say they offer the best risk-return opportunities, behind only investment-grade bonds. But most plan sponsors who took the survey (66%) don’t have any fixed income holdings in emerging markets, while just 25% report that they do. One-third (33%) of those who list emerging market bonds as one of their top two best risk-return opportunities are not currently invested there.