However, in my view, financial theory falls far short of providing all of the diversification needed by long-term investors. Historical experience repeatedly has demonstrated that extreme investment returns—particularly negative ones—are more frequent than theory would predict.

I believe a building block asset allocation methodology is one way to overcome some of the important shortcomings that exist within traditional capital market theory. While this approach draws on theory, it also is tethered to “real world” investment fundamentals.

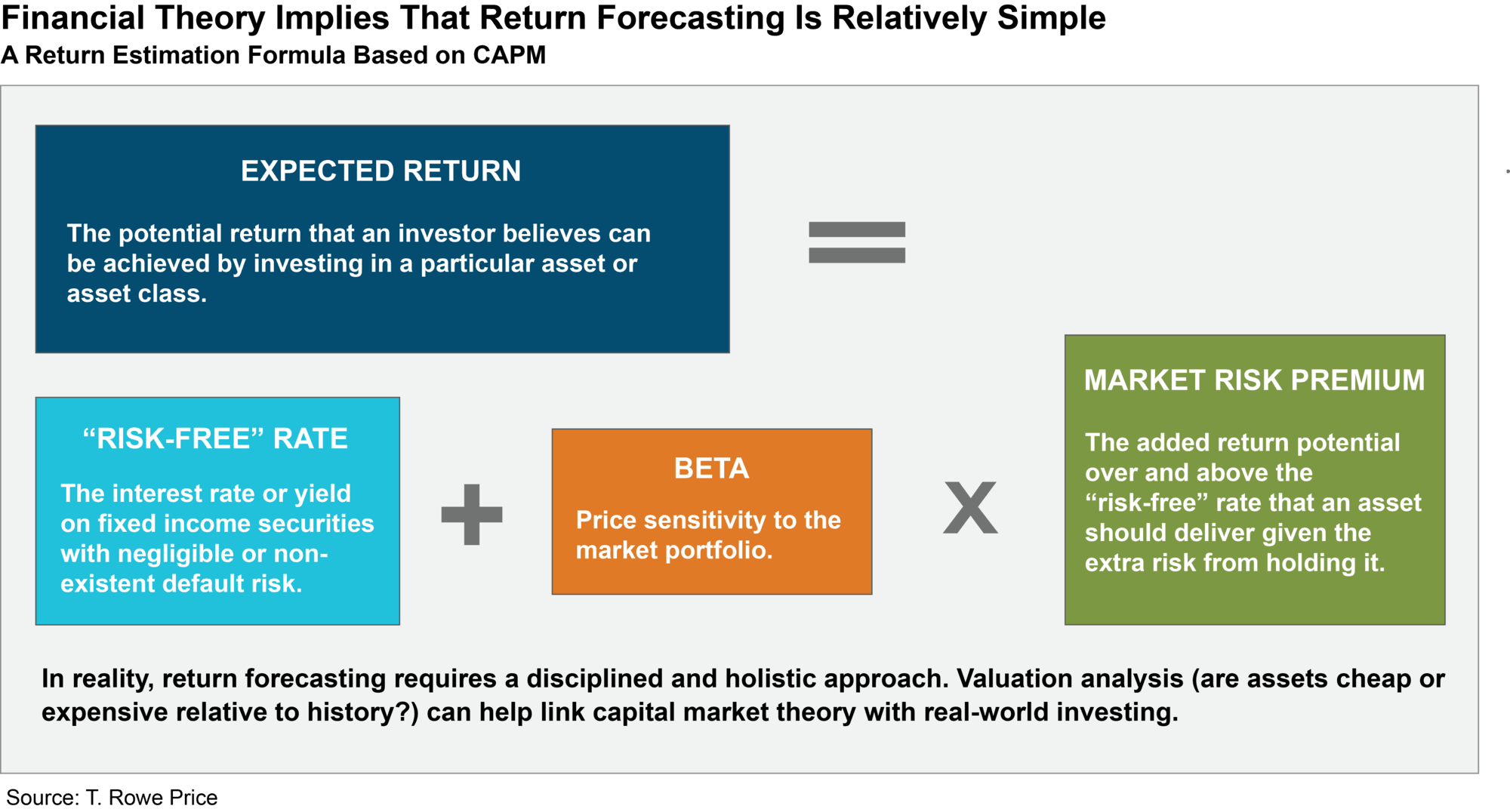

In an effort to improve return forecasts, for example, a building block approach breaks equity returns into three fundamental sources: dividend income, earnings growth, and valuations and their rate of change. By analyzing how historical returns have been driven by these three factors, investors can develop forecasts that don’t rely solely on a CAPM framework.

Building Blocks

I believe the ability to cross-check return forecasts is especially important in the current investment environment. Valuation-based models suggest that returns over the next 15 years will be below longer-term historical averages across a range of asset classes.

By being connected to market data on both an absolute and a relative basis, a building block approach can be used to cross-check return assumptions based on CAPM.