Historically, shorter-term return volatility has been easier to forecast accurately than returns. However, volatility has not always been a good proxy for risk, especially if risk is defined as exposure to loss.

Also, the composition of asset classes can change over time, which impacts the ability to forecast long-term risk. The fact that asset class returns rarely follow a “normal” distribution pattern—i.e., a bell-shaped curve—compounds the problem. Tail risks are difficult to model and forecast.

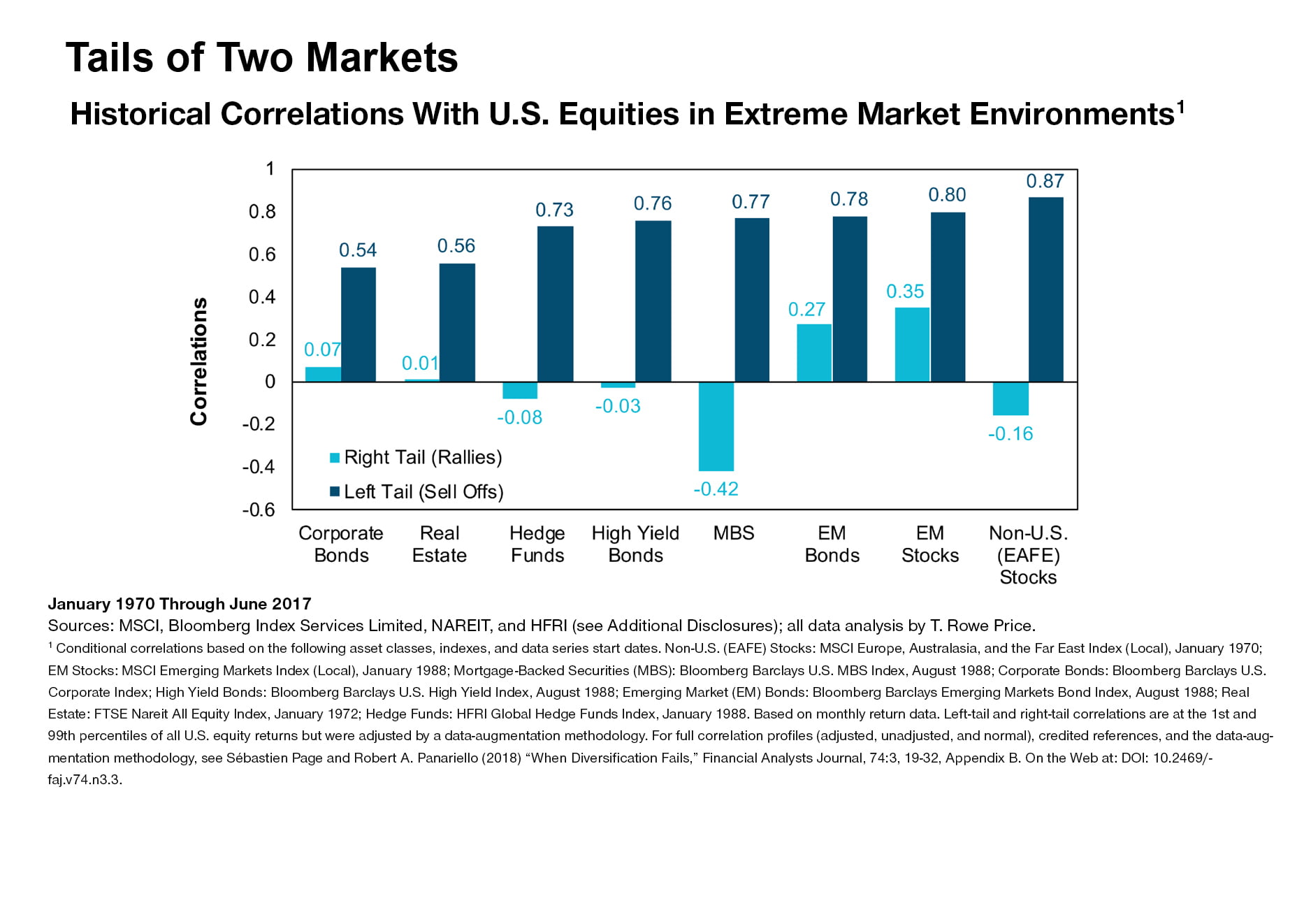

To manage portfolio risk, investors often rely on long-term average correlations when setting portfolio allocations. However, financial markets historically have tended to move suddenly through distinct periods, or “regimes,” of calm and turbulence. Some relatively tranquil regimes have lasted for long periods only to be followed by periods of extreme disruption.

Correlations During Crisis

The problem with shifting market regimes is that investors may believe they are diversified during relatively calm periods, only to find a very different reality when the market mood changes.

While it is an exaggeration to say that all correlations jump to 1.0 in a crisis, correlations historically have tended to spike in disrupted markets. This effect has been pervasive across a variety of assets, including individual stocks, country markets, global industries, hedge funds, currencies, and international bonds.

In 2018, for example, correlations spiked after the Federal Reserve raised its target for the key federal fund rate from 2% to 2.5% and signaled that further hikes might lie ahead. All 17 of the major asset classes tracked by Morgan Stanley Capital International ended the year with negative returns, an unprecedented outcome.