Disruption in its various forms is likely to determine the direction of global markets in the coming year. With the U.S. moving later in the business cycle, the U.S. Federal Reserve raising rates, and credit conditions diverging widely across other global economies, the potential for market volatility remains high.

Although the odds of a downturn appear above average given where we are in the economic cycle, we believe a global recession is a relatively low risk in 2019.

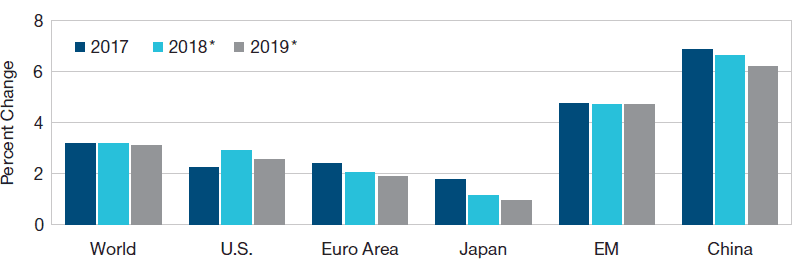

With growth expected to slow in most developed markets, a critical issue will be whether China can restimulate its economy.

October 2018 forecasts by the International Monetary Fund (IMF) projected that growth will slow across the developed markets and in China in 2019. While the U.S. is farthest along in the economic cycle, and the risks to growth are tilted to the downside, a healthy private sector, strong consumer demand, and the lingering effects of the 2017 tax cut stimulus should continue to sustain the expansion through the first half of 2019, T. Rowe Price economists say. European economies are earlier in the cycle, but growth has been slowing since the fourth quarter of 2017, Thomson notes. The UK economy continues to suffer from Brexit uncertainties. In the eurozone, the German labor market shows some signs of overheating, but unemployment is significantly higher in most other continental economies, curbing inflation pressures but also limiting income gains. Efforts by European households to rebuild savings could dampen eurozone growth in 2019.

The IMF forecasts that Japan, which saw economic momentum slow sharply in 2018, will decelerate further in 2019. On the positive side, Japanese corporate profitability is at an all‑time high, according to Thomson, suggesting the risk of deflation has eased.

China’s economic outlook is a particular focus of concern, as official economic reports in late 2018 showed a slowdown in growth. Independent indicators of consumer demand, such as auto sales and Macau casino revenues, also have shown weakness, Thomson says. “What’s crucial is the extent to which China restimulates,” Thomson adds. “Beijing is trying to reduce indebtedness in its corporate sectors. But they do have scope for selective tax cuts in certain areas, or for reducing banking reserve requirements, which is a way of loosening policy as well.” Overall, growth in the emerging markets (EM) is expected to remain stable in 2019, the IMF predicts, with the slowdown in China offset by recoveries in some other major EM economies.

Actual and Projected Real GDP Growth As of October 2018

Source: IMF/Haver Analytics. *IMF projection.

Although U.S. growth is slowing, T. Rowe Price economists expect the U.S. unemployment rate to continue to fall, putting upward pressure on inflation. Higher interest rates, plus a flattening U.S. yield curve, could increase the risk of a sharper economic slowdown in 2020.