Fed rate hikes have fueled global volatility, in part by pushing the U.S. dollar higher. But it’s not too early for investors to prepare for a dollar peak.

2019 may be an excellent time for investors to consider moving some of their fixed income assets into global markets.

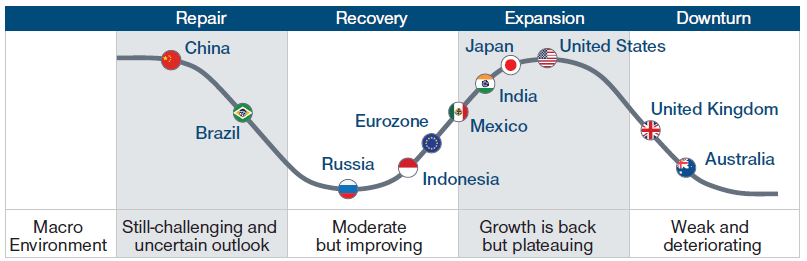

Since the recovery from the 2008–2009 global financial crisis, global credit cycles have grown increasingly out of step. McCormick says he expects that trend to continue in 2019. “Diverging monetary policy is likely to be another catalyst for volatility,” says McCormick. “Markets were simpler to understand when every force was moving in a similar direction. It’s a little bit more interesting now.” The low volatility seen in many major markets in recent years wasn’t sustainable without the ample liquidity provided by the world’s major central banks in the wake of the financial crisis, McCormick contends. Now, with the Fed shrinking its balance sheet and the European Central Bank shifting to a less stimulative posture, “markets are searching for a new footing at more sensible valuation levels given less accommodative monetary conditions.”

Faster U.S. growth and widening interest rate differentials helped lift the U.S. dollar more than 8% on a broad trade‑weighted basis in the first 10 months of 2018. Whether that trend continues or reverses in 2019 will heavily influence the relative attractiveness of international assets—EM assets, in particular. “The dollar exchange rate is crucial,” Thomson says. “Not just because of the currency effect on returns, but because in many markets, a strengthening dollar raises the cost of funding in dollars, which is another form of [monetary] tightening.”

GLOBAL CREDIT CYCLES HAVE DESYNCHRONIZED T. Rowe Price Estimates of Macroeconomic Positions As of October 31, 2018

Source: T. Rowe Price

Relative growth trends will largely determine the dollar’s course in 2019, McCormick argues. If markets perceive that U.S. growth is slowing, they are more likely to believe the Fed is nearing the end of—or at least a pause in—its tightening program.

Stronger growth in the rest of the world also could weaken the dollar. “If the U.S. economy surprises to the upside, or if Italy turns out to be a bigger problem for the eurozone than we expect, the dollar could stay strong,” McCormick says.

However, he adds, “If we do get to a place in 2019 where the dollar stalls, we think that would be an excellent time for U.S. investors to consider moving some fixed income assets into global markets.”