While we believe the fundamental environment remains sound, it’s not improving. As risks are rising, prudent investors may want to consider the merits of positioning portfolios more conservatively.

While we believe the fundamental environment remains sound, it’s not improving. As risks are rising, prudent investors may want to consider the merits of positioning portfolios more conservatively, at least at the margin. Though we don’t think a recession or bear market is imminent, returns going forward may be more muted than they have been over the last couple of years.

The synchronised global economic expansion that powered earnings growth in 2017 appeared to have plenty of steam coming into 2018. However, some indicators pointed to slowing momentum, especially in Europe and Japan.

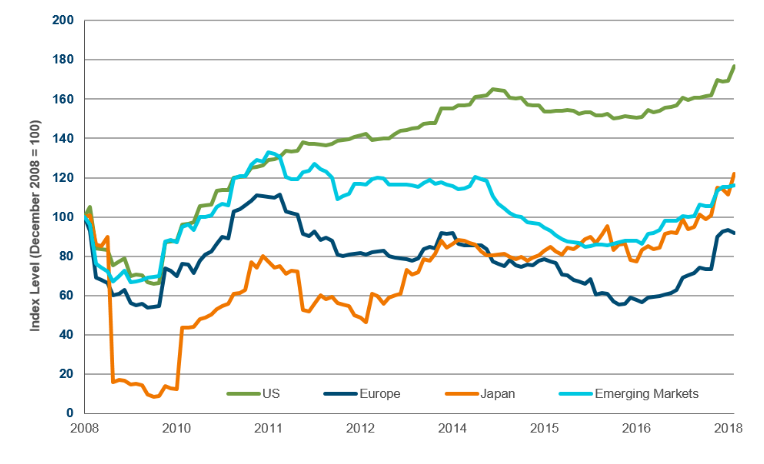

As we enter the second half of 2018, some indicators point to slowing momentum – especially in Europe and Japan (Figure 1). However, it would be a mistake to assume that because the current expansion has been long (nine years and counting) it must be nearing its end.

Rather, we may be at a mid-cycle pause, as central banks around the world recalibrate monetary policy for a more sustainable economic expansion.

Average Monthly Levels, as of May 31, 2018. United States is represented by the S&P 500 Index. Other countries/regions represented by their corresponding MSCI Index. Sources: Haver Analytics [Markit], FactSet Research Systems Inc. All rights reserved.

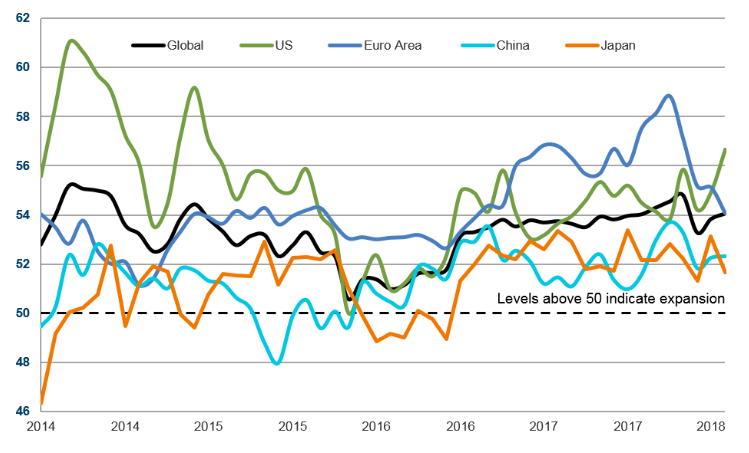

US earnings growth accelerated in the first quarter and although earnings momentum slowed somewhat in Japan, Europe and the emerging markets, underlying trends appear positive (Figure 2). Even if earnings growth moderates over the reminder of 2018, we do not expect a sharp slowdown. This provides a reasonably constructive environment for equities.

Sources: FactSet Research Systems Inc. All rights reserved.

We see three potential headwinds for markets in the second half: rising rates, a stronger dollar, and geopolitical risk.

Most global asset classes appear quite expensive relative to their longer-term averages – averages which themselves have been pulled higher by the equity and bond price gains seen since the global financial crisis.

With global equity markets generally moving sideways in the first half of 2018 despite strong earnings growth, price/earnings (P/E) multiples slipped from their late 2017 peaks. However, higher US interest rates and bond yields eroded the support that extremely low rates have provided for equity valuations since the financial crisis.

Markets are now strongly divided between companies that can demonstrate structural growth and companies that are structurally challenged, meaning aggregate valuations are perhaps less meaningful than they once were.

In this environment, security selection is more important than ever.

Read important information Subscribe for latest news and views