The rise of populism is increasing the risk of a near-term policy shock, and thus of renewed market volatility. While we believe the fundamental environment remains sound, risks are rising.

The rise of populism is increasing the risk of a near-term policy shock, and thus of renewed market volatility. While we believe the fundamental environment remains sound, risks are rising. This suggests that prudent investors may want to consider positioning portfolios more conservatively, at least at the margin.

Markets largely welcomed major policy developments in 2017, including a major US package of individual and corporate tax cuts, the Trump administration’s deregulation efforts, and the election of the pro-growth, reform-minded Emmanuel Macron in France. This pushed global markets to new highs.

In contrast to 2017, 2018 has seen a revival of concerns about a turn towards populism—particularly trade protectionism. Many of these worries center on the Trump administration, which has:

Other political risks include:

In our view, these issues have elevated the near-term risks of a major policy shock, which contributed to the volatility seen in the first quarter. The threat of a US-China trade war is especially unsettling, given that it would involve the world’s two biggest economies. Emerging economies tend to revolve around China, so a meaningful conflict between the two largest economies in the world is a serious risk to markets.

While buoyant earnings helped global equity markets rebound from policy-related “risk off” episodes in the first half of 2018, the US bond market could be more vulnerable. Non-US buyers have accounted for roughly half of the demand at recent Treasury auctions. However, current interest rate differentials also make it possible for Chinese and Japanese investors to purchase German or French government bonds, hedge their currency exposure into US dollars and earn a combined return that in some cases is higher than the yields on comparable Treasuries.

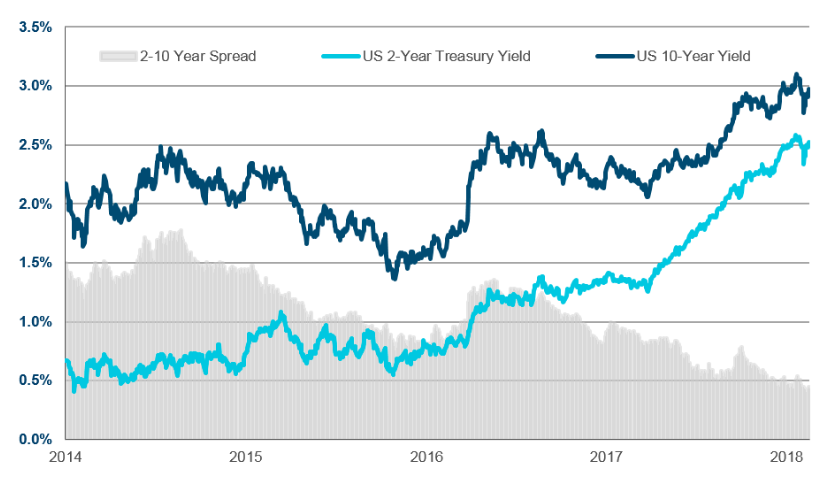

Source: FactSet Research Systems Inc. All rights reserved. As of May 31, 2018 Yields are based on benchmark US Treasury notes

In conclusion, while global growth remains strong, populist policies remain a near-term threat to the world economy. Trade protectionism – particularly a potential trade war between the US and China – may lead to significant volatility in the near term, especially in bond markets. To hedge against political risk, investors may wish to position their portfolios more conservatively as we enter the second half of 2018.

Read important information Subscribe for latest news and views