Tech giants have been the driver of an extended cycle of outperformance for growth investors. Whether growth continues to lead in the second half will depend on the outlook for the global economy, interest rates and energy prices.

A handful of giant tech companies have led the global bull market, thanks to their rapid earnings growth. While privacy and political issues bear watching, we believe the growth potential of these firms outweighs regulatory risks. The tech giants have been the driver of an extended cycle of outperformance for growth investors. Whether growth continues to lead in the second half will depend on the outlook for the global economy, interest rates and energy prices.

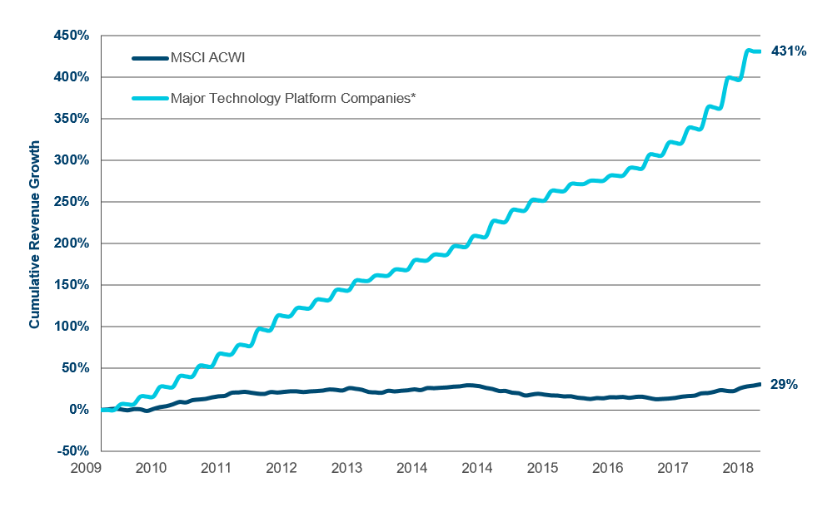

The technology sector continued to lead global equity markets in the first half of 2018. Much of that leadership was concentrated in a handful of US and Chinese mega-cap companies with dominant platforms in internet search, social media, cloud computing and video streaming. Revenue and earnings growth among large tech firms has exploded, far outpacing the broad market.

As of 31 May, 2018. Aggregate revenue growth for the following companies: Facebook, Alphabet, Amazon, Apple, Netflix, Microsoft, Baidu, Alibaba, Tencent. Source: FactSet Research Systems Inc. All rights reserved.

Commanding market positions have allowed these ‘tech titans’ to leverage powerful economies of scale, producing impressive returns for investors. However, they have drawn the ire of some policymakers concerned about data privacy and political manipulation. These concerns flared in early 2018, leading some analysts to speculate that the platform giants might be due for a correction.

In our view, the growth potential of these major tech platforms dwarfs the risk of a political or regulatory backlash. While investors will definitely need to keep an eye on the longer-term risk of government intervention, it certainly hasn't manifested itself in any kind of meaningful change to the trend of increasing dominance and massive fundamental and financial strength.

Tech strength has helped drive relative outperformance for the growth investment style through much of the current bull market―a trend that persisted in the first half of this year. Whether growth continues to lead value in the second half largely will depend on the outlook for economic growth, interest rates, and energy prices. Higher oil prices have boosted the energy sector, while improved net lending margins should support the financial sector as interest rates rise. On the other hand, rate-sensitive value sectors such as utilities, telecommunications and consumer staples could continue to perform poorly.

Ex-US equity markets appear to offer some attractive potential opportunities for value investors. This is especially true in emerging markets, where some large-cap companies that are dominant in their national markets have been shunned by investors because of macroeconomic factors beyond their control. This means investors can buy companies with substantial scale and competitive strengths at prices that are relatively attractive, in our view.

Read important information Subscribe for latest news and views