The global growth outlook has improved following a tepid start to the year, but risks remain on the horizon. Despite this, we believe an imminent recession is unlikely.

Following a strong upswing in equity markets in the first three months of 2019, the mood changed in the second quarter as concerns about the strength of global growth returned. There were several reasons for this, one of which

was a sharp slowdown in corporate earnings growth in the US.

After making gains in 2018, in part owing to US corporate tax cuts, U.S. earnings growth decelerated in the first quarter of 2019. All is not lost, however.

The consensus earnings forecast is for a re-acceleration later in the year, but achieving that result will require faster economic growth, particularly outside the US.

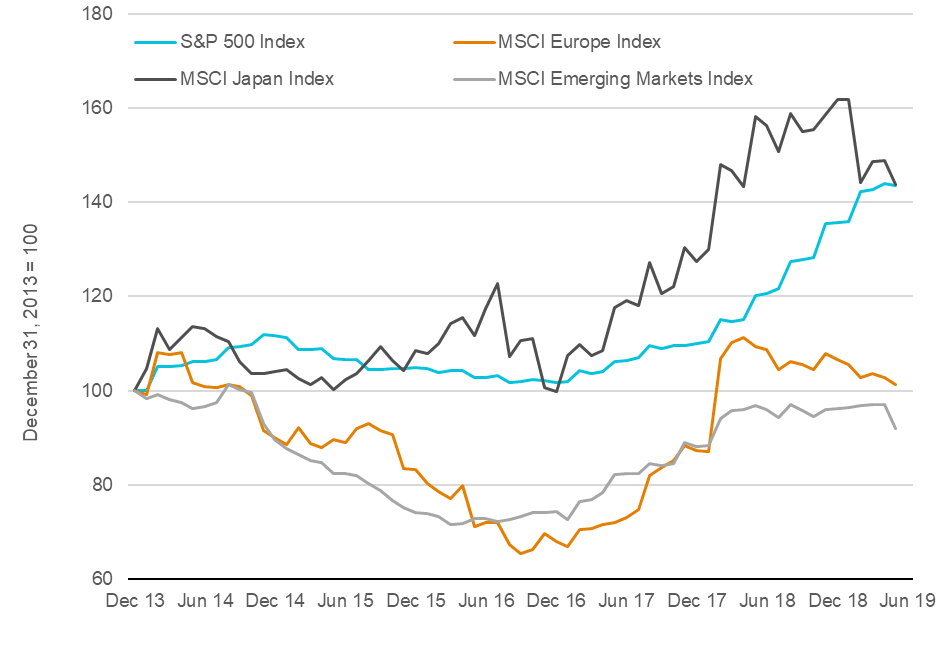

The key challenge, in our view, is that the global economic outlook remains subdued. Most developed economies are growing below their potential, while earnings momentum has turned negative in Europe and Japan.

The strong US dollar is taking its toll on emerging markets, acting as a form of monetary tightening that increases borrowing costs; an unwelcome occurrence for economies that are only just beginning to recover.

Past performance is not a reliable indicator of future performance.Sources: Standard & Poor’s (See Important Information), MSCI (See Important Information). T. Rowe Price calculations using data from FactSet Research Systems Inc. All rights reserved.

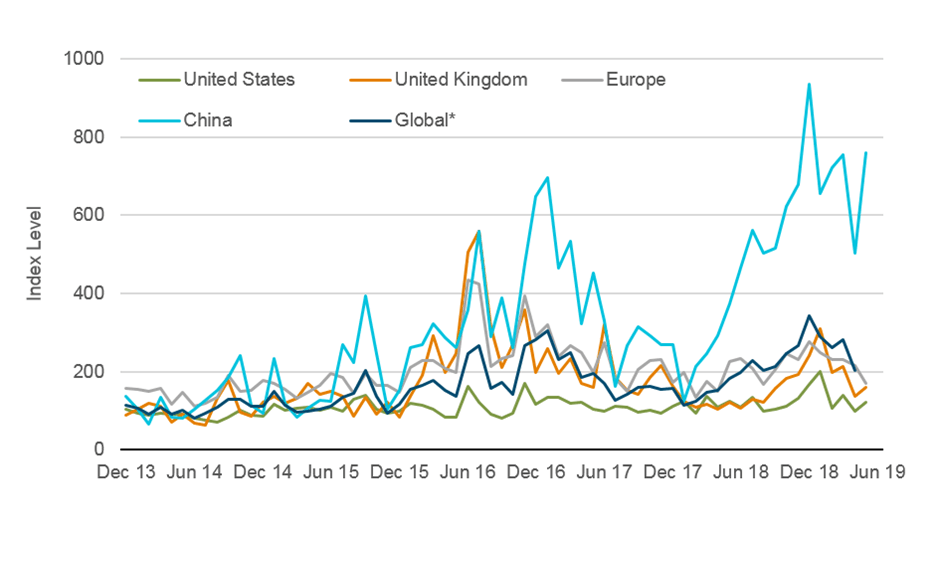

Cumulative growth in earnings per share by region, December 2013 - May 2019

At present investors are facing geopolitical risks from several angles. In Europe, recent elections have shown that populism continues to be a powerful political force. However, trade appears to be the most significant political risk currently facing investors.

As threats of trade wars and tariff hikes have intensified, investors have become more uncertain about the future direction of economic policy. Increased uncertainty can foreshadow a decline in economic growth and employment in following months. Uncertainty reigned in late 2018 as concerns about trade wars dominated the agenda, and it was much the same in May as fears of an escalating trade war came to the fore once again. The US and China exchanged barbs in the form of tariff hikes, the US imposed sanctions against Chinese telecoms giant Huawei, and the Trump administration briefly threatened to impose tariffs on Mexico.

While the US and Mexico managed to reach a deal in June that aims to avoid tariffs, the dispute between the US and China rumbles on. Despite a deal appearing within reach, there are several reasons why neither China nor the US may be in a rush to compromise. In 2020, President Trump faces re-election and may stand to benefit from putting off any agreement until then. Meanwhile, China may believe that denying Trump any success in the negotiations will damage his re-election prospects, allowing them to negotiate with his successor.

Economic policy uncertainty indices, December 2013 - May 2019

*Global Index through April 30, 2019. Source: Economic Policy Uncertainty, policyuncertainty.com. ©2019 by Economic Policy Uncertainty.

During the first half of 2019, financial markets displayed unusual behaviour. On the one hand, falling bond yields and an inverted US Treasury yield curve – where longer-term yields fall below short-term yields – seemingly signalled concerns about slowing growth. Equity markets, on the other hand, made strong gains and appeared to reflect a positive outlook.

At the same time, market expectations for US monetary policy shifted in the first half, which should be positive for investors. With slower growth on the horizon, investors now believe that the Federal Reserve will seek to support markets by cutting rates rather than hiking them further

Yet despite the headwinds that are buffeting the global economy, we believe the risks of an economic downturn, whether in the US or globally, are limited. In our view, at present there is little evidence of any imbalances that would suggest a recession is imminent.

A key variable in this story, however, is China. Growth in the world’s second-largest economy has already slowed, and further deceleration could have a negative impact at a global level. The Chinese government responded to slower growth in late 2018 by easing credit and boosting spending, but the results were not necessarily as positive as desired.

We believe the second half of 2019 will see an environment of positive growth, low inflation, and market pressure on central banks to lower interest rates. This should support further market growth, although we are cognisant that there are several risks lurking over the horizon. With trade disputes and populist politics creating potential downside risks, any flare-ups could be detrimental for financial markets. Any escalation of trade uncertainty could cause global sentiment to fall, dragging down hopes that corporate earnings growth will resume later in the year.

For US equity markets to continue to rise, we will need to see the reappearance of corporate earnings growth. Looking beyond the US, the prospects for equities are also tied to earnings. However, the prospects here look bleak - unless there is a stronger than expected Chinese stimulus.

In bond markets, slow but positive economic growth, limited inflation pressures, and friendly central banks should create a supportive environment in the second half. However, bond investors may wish to take a cautious approach with emerging market debt, which could struggle amid trade tensions and a stronger US dollar.

In this climate, we believe investors are best served by keeping a disciplined, long-term perspective. Holding a globally diversified portfolio will help to smooth any bumps along the way and make the most of potential investment opportunities as they arise.