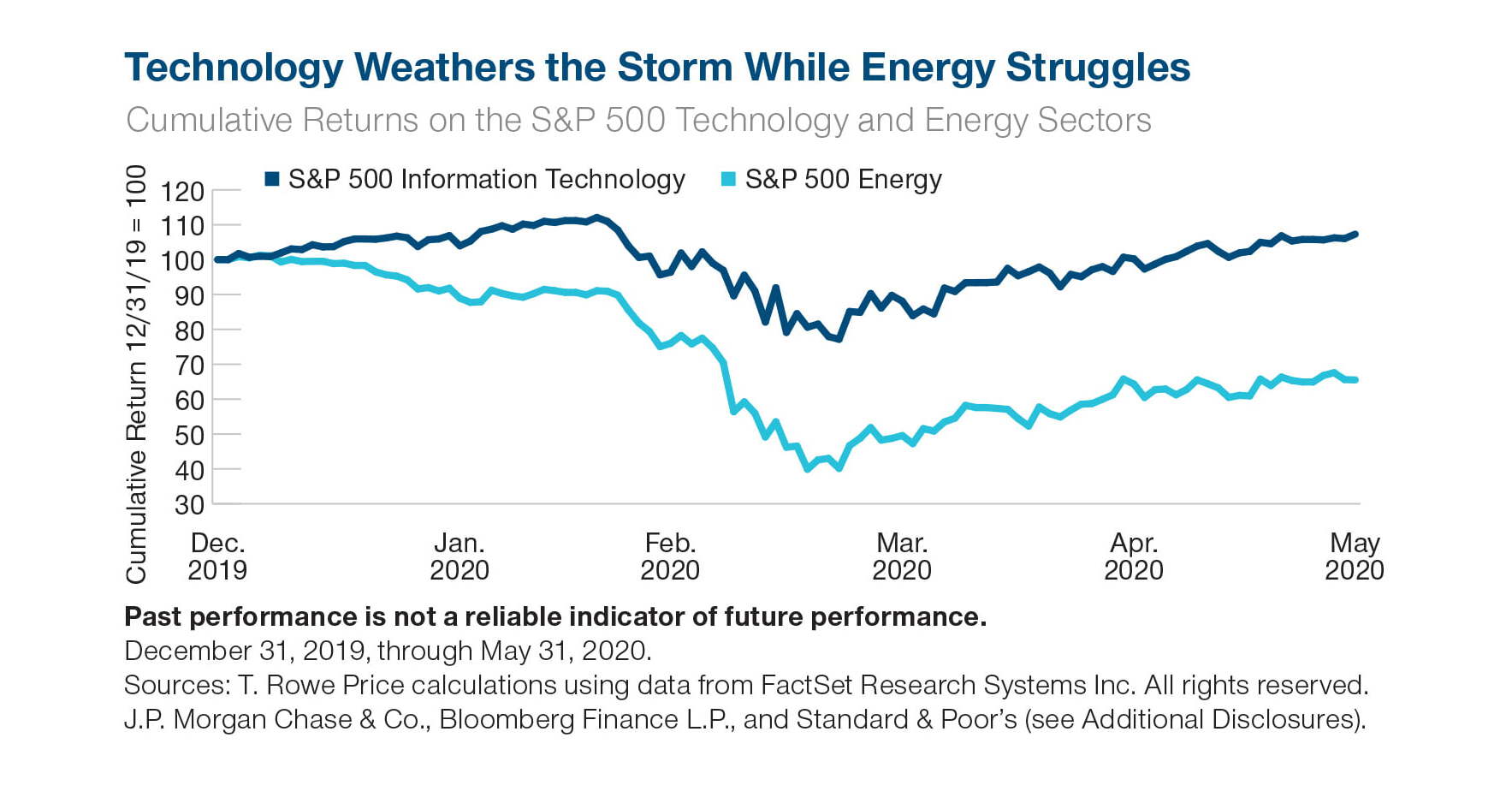

Out-of-favor sectors being disrupted include energy, where new technologies and a price war between Russia and Saudi Arabia have added to supply and driven prices down. In the financials sector, low interest rates and narrow lending margins are hurting banks’ income statements, while rising credit risks are forcing them to hold more capital on their balance sheets. The result is a classic value investor’s predicament: While both sectors are inexpensively valued, they face major cyclical and secular challenges.

“The growth versus value debate slightly misses the point. It’s more complex than that,” says Justin Thomson, CIO, International Equity. “What we have been witnessing over the last 10 years and during this crisis is that free cash flow has been the winning factor. It just so happens that the growth sectors, such as technology and health care, are predominate when it comes to free cash flow, and companies that are more capital intensive have been penalized.”

In this environment, aggregate market valuations essentially have become meaningless, Thomson says, because of the sharp bifurcation between companies that appear to be on the right side of changing trends, and those facing permanently impaired demand.

Sharps says ‘Our team takes a strategic view, as the market begins to recover, we think investors need to use scenario analysis, taking the historical context of each company and sector into perspective. We would suggest pricing in historical normalization, not in the immediate future. And we would urge investors to take the long-term view while carefully and regularly evaluating overall risks.”