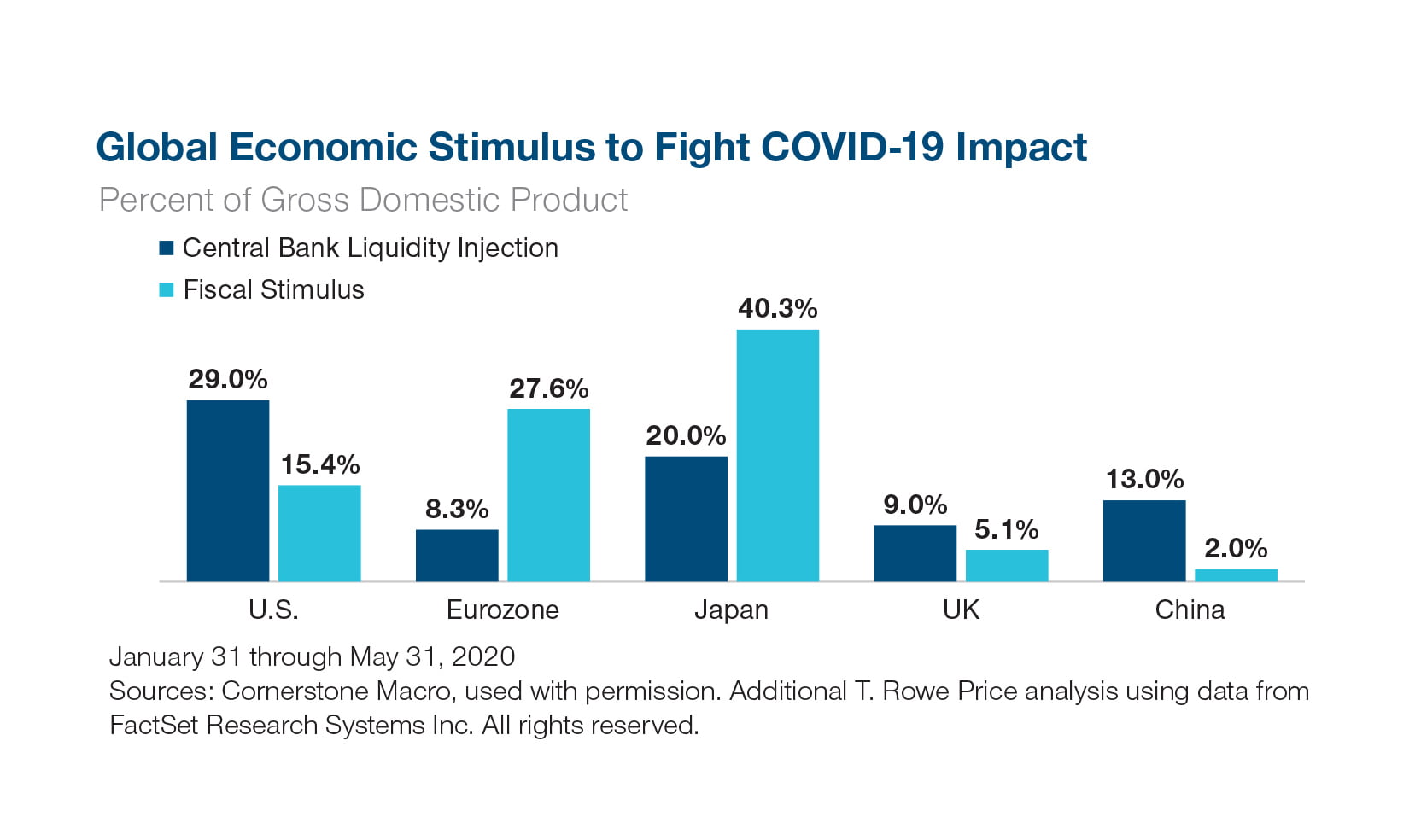

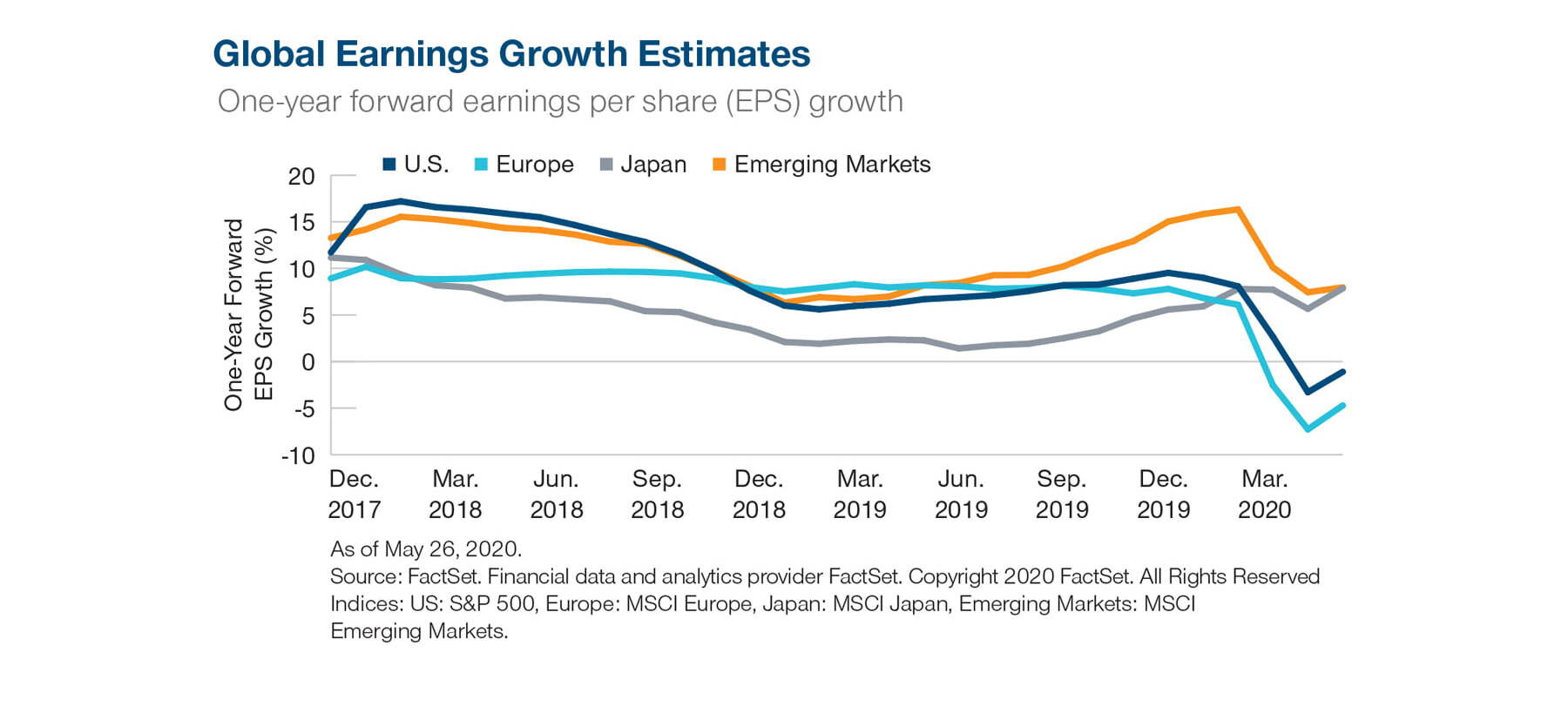

Coming into 2020, the consensus forecast was for 3% growth in U.S. gross domestic product (GDP) during the year. Now, GDP looks likely to see about a 3% decline. Overall corporate earnings could fall as much as 50%-60%. Certainly, fiscal and monetary stimulus have mitigated much of the fallout. The Fed has provided the largest stimulus ever in relation to U.S. GDP. Stimulus efforts also have been well orchestrated globally: through May, fiscal and monetary stimulus efforts equaled 13% of GDP in the U.S., 11% in China, and 10% in Germany. However, amid the hit to consumer demand, it appeared that much of the personal income directly provided by U.S. fiscal stimulus checks may have gone into savings accounts. In the U.S., consumer spending typically accounts for roughly 70% of GDP.

Even as government budget deficits move higher, deflationary forces remain strong. A modest uptick in inflation would help many sectors, but this hasn’t materialized.

Obviously, the recovery’s trajectory will depend heavily on how quickly a coronavirus vaccine and new drug therapies for patients can be developed.

Vaselkiv says there is not a clear path ahead.

“Investors will need to dig deeply to find the green shoots of recovery at the local level, especially employment trends and personal income.”