How has ESG been shaped by the events of the last year? Through varying articles we look at how the pandemic, climate worries, societal division and fights for equality have played out in the world of investments beyond simply the financials. This section includes: • Climate Regulation • ESG Bonds • DEI Spotlight • Public Policy

ESG FOCUS

Maria Elena Drew Director Of Research, Responsible Investing

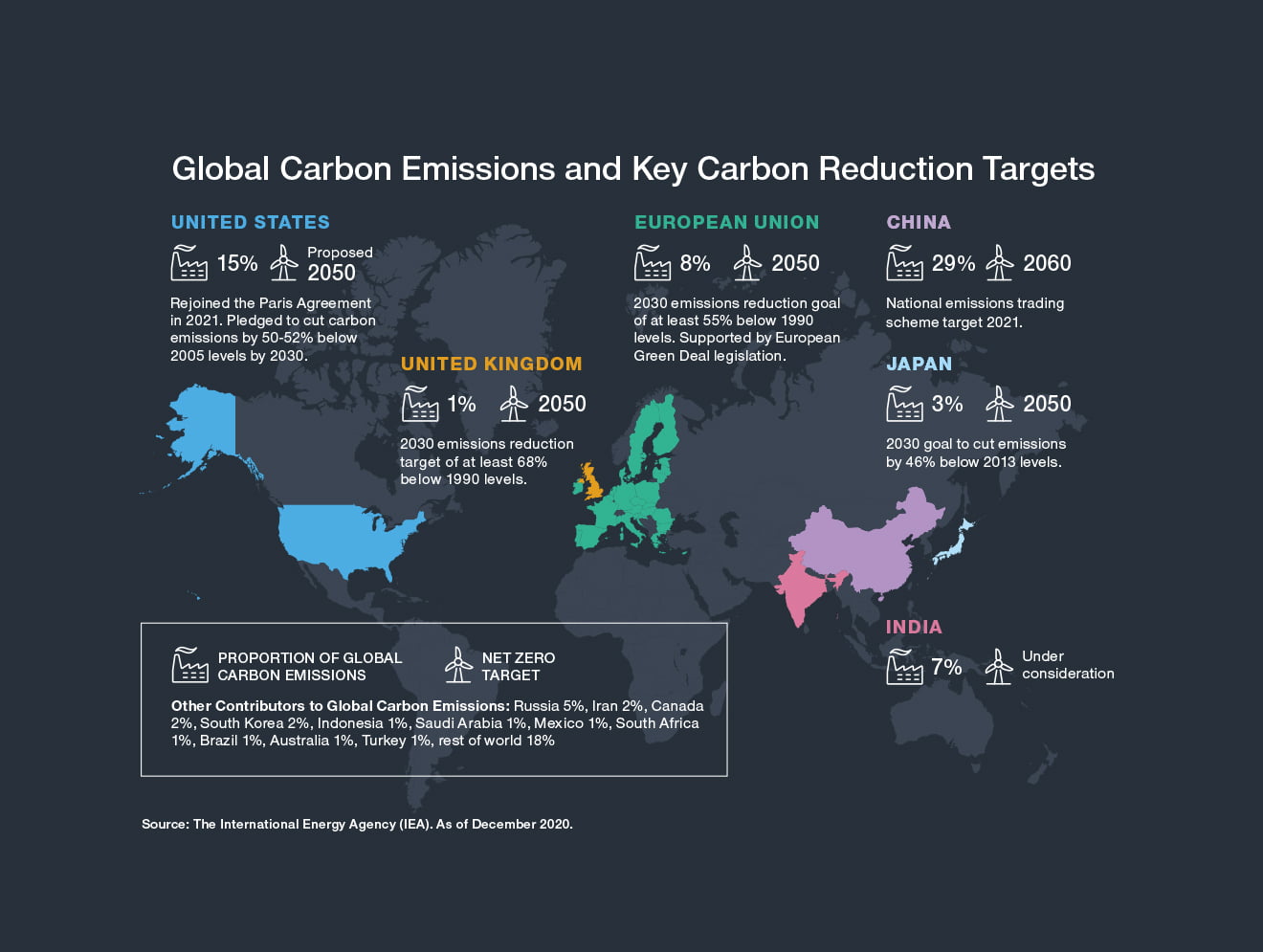

Climate change presents a systemic investment risk, making the importance of an investment’s environmental footprint more critical than ever before. While financial markets are well positioned to play a leading role, ultimately they will only be effective if climate change regulation is in place. We have previously highlighted the mismatch between policy and science when it comes to climate change. Over the past year, we have seen strong momentum to close that gap—a trend we expect to continue through 2021.

In general, direct legislation to underpin net zero targets is largely absent although it appears that the urgency of the situation is increasingly understood. Simply put, the odds of meaningful climate regulation coming into force is very high. To put the potential impact of forthcoming regulation into perspective, most estimates indicate that the world’s current climate change commitments put us on a path to 2.7°–3.0°C of global warming. At this rate the probability of staying below 2°C warming is only 5%, but if all countries were to meet their nationally determined contribution power targets, it rises to 26%.1

HOW CLIMATE CHANGE AFFECTS FINANCIAL PERFORMANCE As new rules come into effect globally, we expect that performance around climate issues will become increasingly more important to investment performance. Beyond regulation changes, innovation and consumer preferences are growing factors helping to move the needle on how companies are responding to climate change. Innovation such as advances that have driven down costs in renewable power and sped up deployment of renewable capacity, means current Nationally Determined Contributions (NDCs) for 2030 should be met as soon as 2022. Consumer influence can be seen through companies adding environmental labeling to products, as well as an increasing demand for more sustainable products, such as meat alternatives.

EVALUATING CLIMATE CHANGE IN INVESTMENTS Our evaluation of climate change factors focuses on energy transition and physical risk, but we believe an issuer’s environmental footprint and track record are also important indicators of how they may perform in a tightening regulatory environment. With our RIIM assessment, we consider our investments’ environmental characteristics holistically—key areas of focus include:

Climate change is increasingly a major concern for global communities, companies, our clients, and our investment teams. The focus on how companies are working to mitigate the risks to their activities is only set to intensify, and 26th United Nations Climate Change Conference (COP 26) and regulatory efforts will bring the issue further into the spotlight.

1 Liu & Raftery, Country-based rate of emissions reduction should increase by 80% beyond nationally determined contributions to meet the2°C target (Nature 2021).

Matt Lawton Sector Portfolio Manager

In 2020, $512 billion of ESG-labeled bonds were issued—an increase of 67% over the prior year.1 Capital-raising to address pandemic relief efforts drove much of this increase. The largest proportion of ESG-labeled bonds continues to be green bonds, but 2020 saw social bonds and sustainability-linked bonds grow their share substantially. ESG bonds generally trade at a premium to their non-ESG counterparts, making them a cheaper way for issuers to borrow. Demand pressures from passive funds with ESG benchmarks and green bond mandates have helped create a situation where the greenium effect is applied almost uniformly across the bond market, despite the actual environmental and social credentials underpinning each bond. We are encouraged that companies are undertaking the green and social projects eligible for 1. Bloomberg Finance L.P.

ESG-labeled bond financing. However, we need more than a label to validate the environmental or social credentials of a bond. We have concerns about some of the issuance practices around ESG-labeled bonds. Specifically, we are concerned about bonds lacking “additionality” (i.e., issuing a green bond for operational expenditures on renewable energy procurement that was already taking place). We’re also concerned about various sustainability-linked bond structures. Some of these allow an issuer to recall the bond before sustainability target dates or where the step-up for meeting the target is immaterial.

We leverage our RIIM analysis and fundamental research to evaluate the issuer as well as its ESG-labeled bond framework. We focus on the credibility of the use of proceeds and the quality of the post-issuance reporting. We also look for alignment with industry standards and whether the issuer has obtained external verification.

Donna Anderson Head of Corporate Governance Maria Elena Drew Director Of Research, Responsible Investing

FROM TRAGEDY COMES GREATER COMMITMENT TO IMPROVE ON EQUALITY DIMENSIONS Amid the tumultuous markets of 2020, another important investment movement arose from a tragedy of a different kind. The concern of investors and other stakeholders around diversity, equity, and inclusion (DEI) amplified following the tragic death of George Floyd at the hands of Minneapolis police in May 2020. It compelled corporations to examine their links to systemic racism and explore ways to change these persistent and destructive patterns.

COLLECTING DATA ON DIVERSITY, EQUITY, AND INCLUSION We have four ways to generate insights about DEI and corporate culture.

1 Investment analysts’ fundamental research and analysis of the companies they follow.

2 Proxy voting guidelines that address board diversity specifically.

3 ESG corporate engagement program.

4 Proprietary Responsible Investing Indicator Model.

Even with these steps, a lack of available comprehensive and comparable data in this area remains a serious challenge.

Disclosure levels by companies around DEI issues as of the end of 2019 were not impressive. Even for the large-cap S&P U.S. equity universe, the levels of disclosure on gender diversity in management and within the broader workforce were poor.

Encouragingly, we think the trends are improving, as dozens of larger U.S. companies have already agreed to accommodate investors’ demands for more detailed diversity information.

RACIAL INEQUALITY: A CONTINUUM OF RESPONSES In our recent discussions, we have observed that corporate reactions to stakeholders’ concerns in relation to DEI have fallen along a continuum, as illustrated in here. While there is no single correct response, we believe that companies that make substantive changes to promote workforce diversity will have better outcomes in the long term.

What is clear already is that DEI is a core value for many stakeholders of these companies—current and future employees, customers, investors, leaders, and boards. Those companies that do not meet stakeholders’ expectations will likely see an erosion in their ability to compete for talent and market share.

We had 633 ESG-focused engagements in the second half of 2020. 58% of these featured DEI on the agenda. It was evident to us that corporate reactions to stakeholders' concerns in relation to DEI have fallen along a continuum.

Katie Deal Analyst, Washington and Regulatory Research

CONCERNS AROUND U.S. POLICY REMAIN, BUT OF A DIFFERENT NATURE Between 2016 and 2020 we saw a marked increase in concern from investors regarding the political volatility driving the legislative and regulatory environment.

More recently, investors have expressed concern regarding the legislative and regulatory backdrop, but for an entirely different reason: crisis management.

U.S. President Joe Biden adapted his policy rhetoric from “transformation” to “crisis management,” framing the federal government as a source of stability for American families and businesses—not only for the dual public health and economic crises, but also for the risks that climate change and racial inequality pose.

The Biden administration’s foremost priority is helping the nation heal from the public health and economic fallout caused by the coronavirus pandemic. These changes would have dramatic implications for different sectors’ recoveries and will likely shift investors’ overall expectations regarding tax policy, gross domestic product growth, and inflation.

A comprehensive, progressive environmental reform package like the Green New Deal is unlikely in this presidential term.

However, we should expect a significant reversal from the regulatory status quo as President Biden seeks to build one of the most progressive environmental policy portfolios in U.S. history.

We also anticipate that the Biden administration will pursue stronger disclosure requirements and assessment of climate risk from firms.

President Biden has explicitly identified racial injustice as a pivotal crisis facing the United States, intersecting with issues like wealth inequality.

We should expect the administration to pursue labor reforms, regulations and policy developments that improve racial equity while also addressing workers’ rights. Congressional gridlock may prevent the Democratic majority from achieving several of these goals, including their progressive corporate and personal tax proposals.

After the January 6 attack on the U.S. Capitol, there was a renewed push for technology regulation. The ramifications of such regulatory actions on the operations—and the bottom lines—of those companies most impacted could prove substantial for investors.