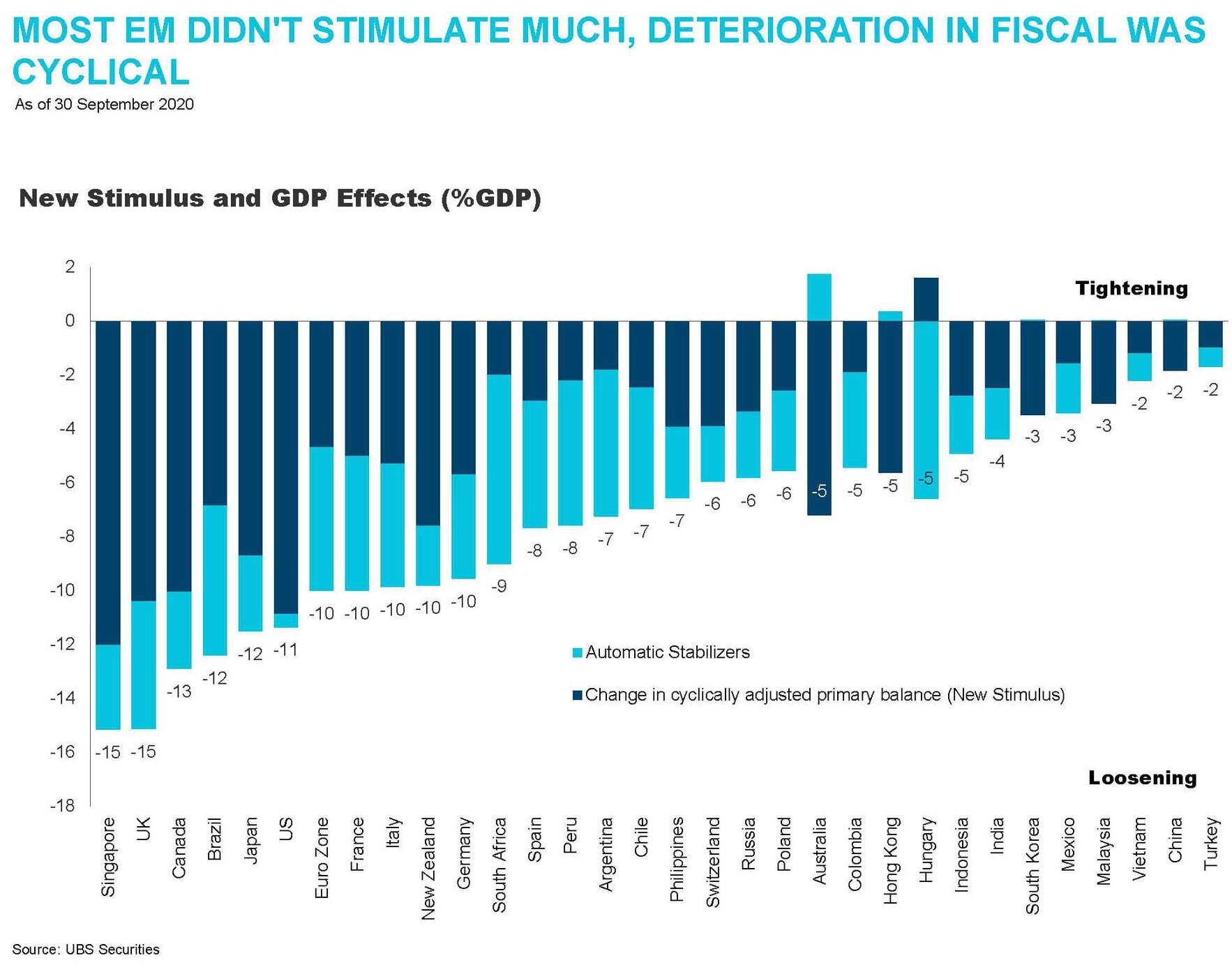

As “stay-at-home” orders became the standard around the world during the onset of the COVID-19 pandemic, global economies were effectively brought to a standstill. Cyclical and capital-intensive industries were particularly impacted, and these industries are highly important to EM economies and their trade activity. Some regions, such as North Asia, were more rigid in their shut down practices. Other regions, like Latin America, could not afford to fully shut down their economies, and they suffered a higher initial infection rate as a result.

A halt on global trade weighed heavily on EM fiscal balances and foreign exchange. But as public health conditions continue to improve globally and trade continues to return to pre-COVID levels, we expect a cyclical recovery in EM, supported by measured stimulus efforts, household savings, the return of corporate capital expenditure and strong corporate fundamentals.

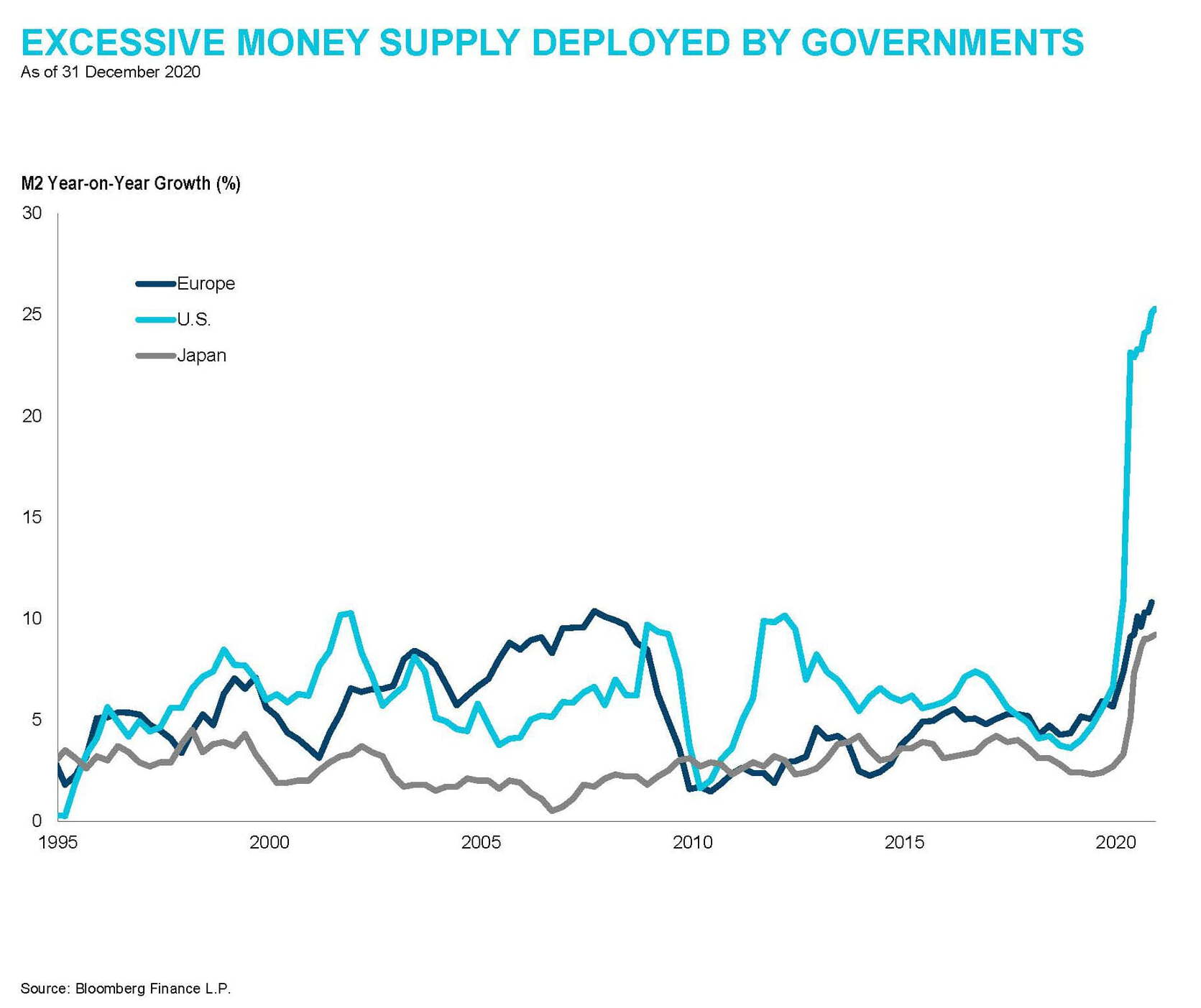

In our view, governments are changing their stimulus measure responses, veering away from traditional quantitative easing and instead targeting consumers directly. This structural change in stimulus policies should result in a more visible multiplier effect, which should benefit beaten down sectors and value stocks.

On the geopolitical front, we will be monitoring the economic policies that the Biden administration embarks upon. U.S. fiscal policy will have an impact on the value of the U.S. dollar against other currencies, which in turn has a considerable bearing on the performance of EM.