2025 Midyear Market Outlook

Investing in a post-globalisation world

2025 Midyear Market Outlook: Investing in a post-globalisation world

Trump's tariffs will hit the US economy hardest in the near term

Equity markets to broaden

further

Bonds with credit risk may outperform government debt

Inflation protection and equity diversification to drive asset allocation

Important Information

Thanks for reading

2025 Global Market Outlook - Investing in a post-globalisation world

The year 2025 was always going to be one of change, but the speed and extent of developments have taken almost everybody by surprise. The full impact of trade policy shifts has yet to unfold, but it is clear that the global trading system is being reconfigured before our eyes, with profound implications for financial markets.

We are undergoing a process of deglobalisation. This will negatively impact the global economy, with the key protagonists, the US and China, hit hardest. It is also a key factor in our outlook for equity, fixed income, and asset allocation investing through the rest of 2025.

The threat of tariffs has brought forward changes in equity markets that had already begun to occur prior to November’s US presidential election. The spread of earnings growth between the “Magnificent Seven” group of mega‑cap tech stocks and the rest of the US stock market will likely continue to diminish, fuelling a period of less concentrated markets and more varied market leadership. We expect this broadening of the opportunity set to include non‑US stocks as well.

In bond markets, massive German fiscal expansion, in combination with the US tariff policies, has triggered a global regime change. Higher‑trend inflation—most notably in the US—and a heightened risk of a sharp growth slowdown are pushing developed market sovereign bond yields higher, eroding the quality of developed market sovereign bonds. However, corporate bonds are heading into the difficult period ahead with meaningfully higher overall credit quality than in the past.

The market environment has led our Asset Allocation Committee to favour inflation protected bonds and real assets, such as real estate and commodities, to offset inflation risk. Given the likelihood of continued geopolitical volatility, we are focusing heavily on valuations and continue to favour value stocks overgrowth stocks. We also modestly favour non‑US stocks.

Volatility is elevated, and policy is changeable. We are ready to respond as clarity over tariffs emerges over the coming months. The most important thing is to acknowledge that in the less globalised world ahead, the range and mix of investment opportunities will be different from those to which we have been accustomed. Successfully adjusting to this new reality will demand heightened vigilance, a willingness to let go of old assumptions, and an ability to take decisive action when required.

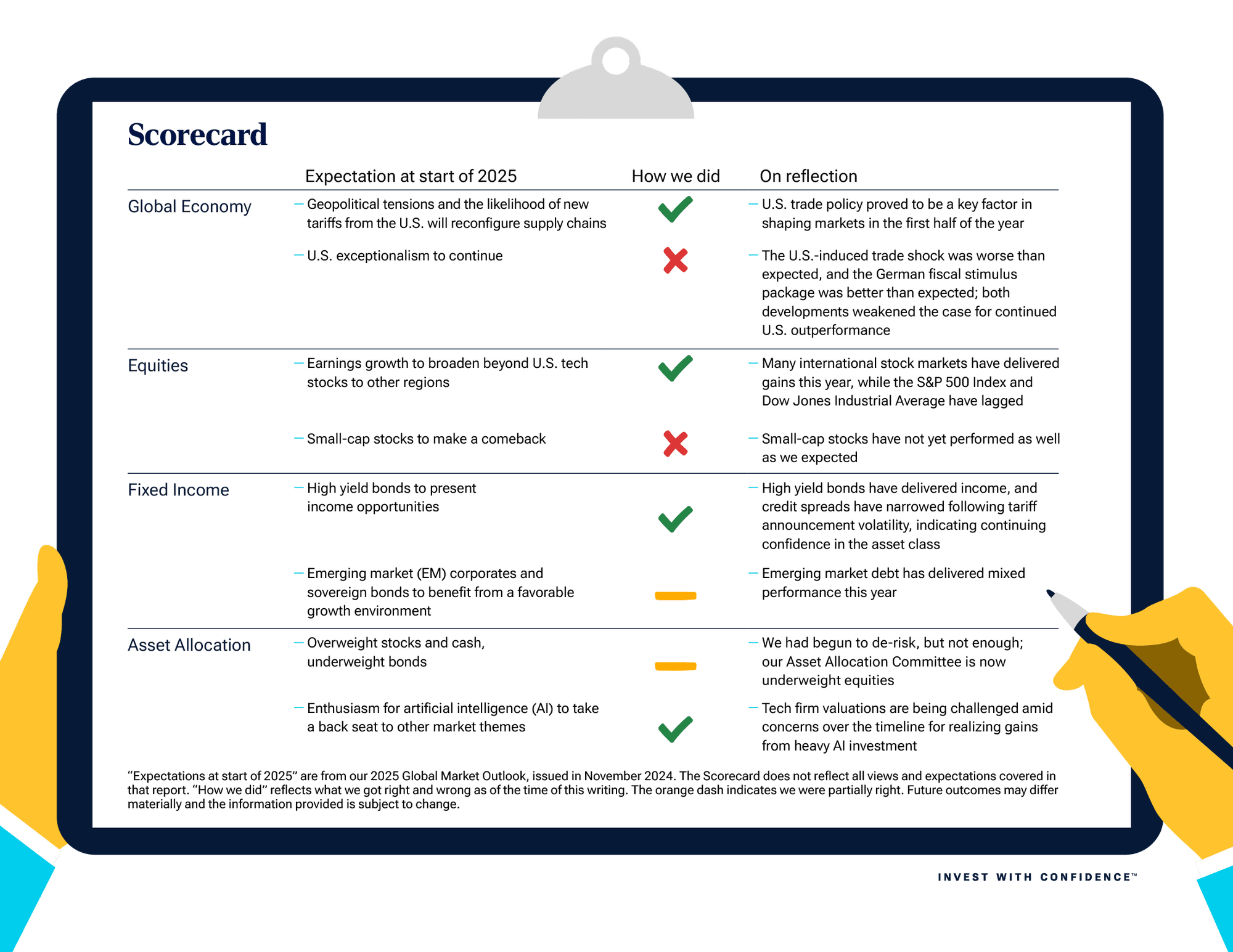

Go to the next page to see our scorecard where we are revisiting our expectations for 2025 by looking back at some of the predictions we made in our 2025 Global Market Outlook last November and scored ourselves for accuracy based on where we are today, almost halfway through the year.